|

|

发表于 30-8-2016 11:16 PM

|

显示全部楼层

发表于 30-8-2016 11:16 PM

|

显示全部楼层

你手上還持有hevea?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 12:24 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 01:20 PM

|

显示全部楼层

你手上还有吗 我在等 0.85-0.90 的时候进场

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 03:08 PM

|

显示全部楼层

哭哭也是没有了..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 03:12 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 05:22 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 05:41 PM

|

显示全部楼层

你是玩基本面還是技術面的?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 31-8-2016 06:13 PM

|

显示全部楼层

还以为你有持有,,哈哈。现在你持有什么股票?可以分享吗?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 2-9-2016 12:29 AM

|

显示全部楼层

本帖最后由 icy97 于 2-9-2016 01:27 AM 编辑

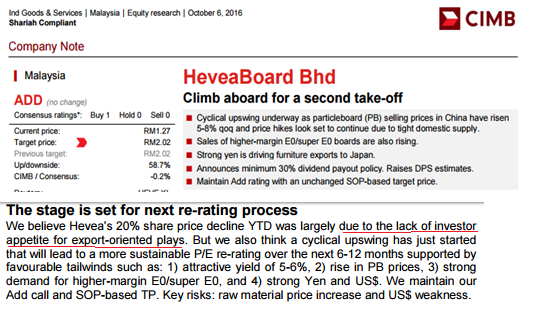

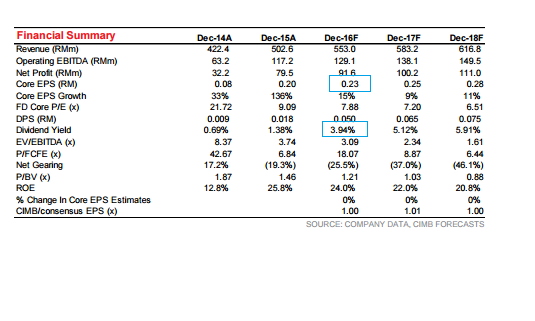

買進券商心頭好‧令吉貶值有利億維雅 下半年業績料更佳

2016年9月01日

http://www.chinapress.com.my/20160901/買進券商心頭好‧令吉貶值有利億維雅-下半年業績/

券商:聯昌證券研究

合理價:2.02令吉

億維雅(HEVEA,5095,主要板工業)工廠于次季關閉進行維修,相信下半年將有更強勁業績表現,至于每股1.3仙股息亦稍高于市場預期,加上令吉貶值,將是該股潛在重估催化因素。

在家具業務推動下,該公司上半年營業額按年攀升18%,稅前淨利按年起29%。同期,夾板營業額增5%,淨利跌10%,主要受工廠關閉維修影響;家具業務營業額漲27%,淨利在較高美元兌令吉匯率,以及自動化改善下倍增。

按季比較,該公司營業額跌17%,稅前盈利下滑24%。該公司每股淨現金從截至首季的每股20仙,于次季增至每股25仙,占現有市值的21%。

億維雅首季償還4500萬令吉,相等于1100萬美元的美元計價長期貸款,因此相信下半年可有強勁派息。

值得關注的是,該公司于次季沒有匯率虧損,這是過去一直拖累營運淨利的因素。

億維雅本季宣布派息1.3仙,稍高于市場預期,我們相信每個季度派息1仙,全年派息4仙的預測仍屬保守。

我們維持億維雅“增持”評級,目標價為2.02令吉,令吉升值為主要下行風險。令吉兌美元每升值1%,將降低該股2016財年每股盈利預測7.5%。該股潛在重估因素,包括令吉貶值及高于預期的派息率。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-9-2016 01:42 AM

|

显示全部楼层

本帖最后由 icy97 于 22-9-2016 02:55 AM 编辑

[分析冷眼大师选股] NO.2 HEVEABOARD BERHAD

Author: GoldenEggs | Publish date: Wed, 21 Sep 2016, 04:18 PM

http://klse.i3investor.com/blogs/Goldeneggs/104806.jsp

今天继续分析第二支冷眼大师大量持有的股,总共持有八百万令吉(包括HEVEA-WB), 其实大师已经在这个公司赚了很多,可能当初投资时成本不到一半,所以说每一支他所投资的股我都会从基本面去学习。

HEVEBOARD 是一家生产particle board 和 ready to assemble products 的工厂,简单来说就是一家板厂。最近几年生意可以说是好得不得了,从2012年净利15.4M到近一年的79.24M (+520%) 的上涨。看到这里大家肯定觉得股票也从0.5飙升到5.08(1 split 4 )。但是从我的估算中,HEVEA仍然是极度被低估,可以说是bursa中排名第三被低估的股票。很大的原因在于管理层被网友抹黑操纵股票。这也让我们有机会买进一支便宜且优质的股票。

好吧,基本面来了。。。PE: 7.30 (对一支成长股来说夸张的低),Dividend Yield 方面就略低了,不到2%但我是觉得既然管理层能善用资金来赚更多钱,那就拿少一点吧。效率方面,41.5% 的Return On Invested Capital (也就是公司一年所赚的钱除以所投入的成本),这很清楚说明了HEVEA 呢是一支非常节省成本且很擅用公司的资金,也可以从这里看得出为什么冷眼大师持有数会比第一篇的SUPERLON多了。

FreeCashFlow/Market Cap 方面呢, 达到了22.6八仙,足足是定存的4倍多,CASH ROIC 更是46.5%。我想你们看到这些数据也不敢相信这是真的吧。HEVEA 目前是一家net cash company (98.76M) 的net cash, 相信风暴来时对公司只是小挑战。这些都是以HEVEA 这一年的盈利计算的,看了以上数据,大家应该明白为什么HEVEA会是第三被低估的股票了。

总结:HEVEA 是一间 NETCASHCOMPANY,非常会擅用资金,效率一流,有野心。我对他的估算在3.02到3.20之间,非常的被低估,你们可以使用你们持有的公司的基本面来比一比就知道了。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-9-2016 01:44 AM

|

显示全部楼层

本帖最后由 icy97 于 22-9-2016 02:58 AM 编辑

Hevea: Should I sell with these negative sentiments?

Author: kcchongnz | Publish date: Mon, 19 Sep 2016, 09:55 AM

https://klse.i3investor.com/blogs/kcchongnz/104613.jsp

“K C, what is your view on Robert’s adverse posting on Hevea in i3investor”

A course participant asked me on August 30 2016 when Hevea’s share price was wacked down by more than 10% to RM1.05 from RM1.20+ in just a couple of days.

“Avoid following rumours and baseless accusation and just focus on the fundamentals”, I said.

Yes, what we read from bloggers we have to take it with a pinch of salt, in fact, it should be a handful of salt as there are all kinds of rumours, half-truths, lies and more lies in the internet. You are fortunate that you have learned the language of business and you should be able to evaluate if the second 2016 quarterly results were bad as claimed by Robert, without any justification. You can also evaluate the value of the company, using the various valuation techniques that you have learned and come out with a range of values, and also take a peep in the future of the business of Hevea. I am pretty sure you can come out with better judgement on your own.

“K C, what you say Tan Teng Boo has a target price for hevea at 60 sen, half its share price now?”

That was another question asked by another course participant a couple of months ago when we had a drink at Sunway Pyramid. I didn’t pay much attention to it then but this issue was raised again by a few more participants in our WhatsApp group just a couple of days ago. This time, I think I must look at how TTB has come out with his target price of 60 sen as this is a huge deviation of my estimated value. TTB is a pioneer in value investing in Bursa, I thought we should pay heed to what he says. In investing, it pays to look at other people’s point of view too. I got a copy of icap’s report from one of my participants.

My previous analysis

Five months ago I have written about Hevea as a stock pick in this service when it was trading at RM1.17. I have done detail analysis and given you a comprehensive report about my investment thesis. Its share price has risen a little, not much, but with the dividends, the total return is about 10% now, which is satisfactory in this short term, in my opinion, although the long-term return is what we are looking for. Appended below was my conclusions in my report.

[Conclusions

Hevea, in the past few years, has transformed itself from a very risky company with huge debts facing a financial crisis in 2008 to a highly profitable and safe company with net cash now. It exhibits high growth in recent years and earns high return on capital with excellent cash flows and free cash flows. In another words, Hevea has transformed itself into a great company.

The investment thesis of Hevea lies in its low market valuation with earnings yield of 19.3% and its high cash yield of more than 10%, more than twice that an investor can get from putting his money in bank fixed deposit.

The conservative GCGM with growth assumption just matching the rate of inflation shows that Hevea is worth RM2.18 per share, or a margin of safety of 46% investing in it at RM1.18.

I see little risk in investing in a good company at a cheap price, but potential in extra-ordinary gain.]

The intrinsic value of Hevea of RM2.18 has taken into the dilution effect of the warrants using the Black-Scholes OPM in my analysis. There won’t be significant difference if you consider the warrants are fully all converted as the warrants are deep in-the-money now. But how come there is such a huge discrepancy between my valuation and that of TTB, bearing in mind that we both follow fundamental value investing.

Let us have a look at what TTB’s analysis and report is on Hevea as shown in his report. It is either I was overly optimistic or he is too pessimistic. It is the two ends of extreme.

Icap’s evaluation on Hevea

For sure icap has very good qualitative analysis about Hevea, and for most companies they analyze. This is understandable as they are the professionals and this is their rice bowl. We can’t get near to them.

Reading through the report, I see many positive points mentioned by icap on Hevea. These are:- In house R&D capability

- Products mainly export to Japan, China, Korea etc. of 80%-90%

- Huge improvement in efficiency in RTA especially

- Huge improvement in asset turnover the last couple of years. It means sell more.

- huge increase in revenue and profit

- Huge improvement in balance sheet and in net cash

These were basically what I had seen. Why not, as we both follow fundamental analysis.

But why the target price of 60 sen?

Dear course participants, I am afraid you have interpreted wrongly what icap is saying. It never says the target price of Hevea is 60 sen if you read the report thoroughly. it merely mentioned that,

"Based on these, icap rates Hevea as a Buy at below RM0.60 for long term"

Anything wrong with the above statement by icap? I don’t think so.

You were taught as value investors. We should only buy a stock when it is selling at a wide margin of safety, weren’t you? TTB has always been very consistent with his opinion, that the market is heading for a crash since some years ago, and hence his low recommended buying price, in any stock he analyzes now. He, however, didn’t come out with any valuation of Hevea and we don’t know what intrinsic value he has for Hevea, 20 sen, 30 sen? We don’t know. But we do see a glimpse of its opinion on Hevea in its conclusions as shown in points form below.- “At RM1.21 and with warrants outstanding, Heveaboard is capitalized at RM662.2m. for this what do investors get in return?”

- “With the majority of sales coming from exports, currency fluctuation has a significant influence on revenue”

- “While lowering cost through higher automation, the company is currently focusing on margin growth through the sale of low formaldehyde emission products and equipment upgrading.

- Although this is a good strategy, without an adequate expansion of PPE, the company’s growth will eventually be hindered.

I will try to give my opinions on icap’s concern as below:

- With a market cap of RM662.2m, it is only selling at a price of 7 times net earnings, enterprise value of just 4.8 times its Ebit, and a high cash yield befitting a No-brainer Investment of close to 10%. After taking the full dilution of its warrants into consideration, Hevea is still selling at 45% below my estimate of its intrinsic value from a conservative Gordon Constant Growth Model using an average FCF for the last 5 years to be conservative. Its FCF last year was two and a half three times more than this average.

- I have no predictive power about the future direction of Ringgit versus say USD. However, I think it is not easy for Ringgit to rise up to RM2.50 to one USD like 30 years ago, and hence hamper the export companies like Hevea. What do you think is the likely the direction of Ringgit against USD?

- Isn’t this equipment upgrading a form of capital expenses which have had shown good outcomes?

- I think we will leave them to the management which should know better than anyone else.

Second quarter 2016 results

Hevea reported its second quarter 2016 results at the end of August. Revenue for the half year increased by 18% to RM268m and net profit by 15% to RM35.4m compared to the corresponding period last year. Free cash flows remained strong at RM30m for the 6 months. Needless to say, the balance sheet continues to improve with net cash now at RM100m, up from RM67m at end of last year. As a result of this good FCF, a first interim dividend of 1.3 sen was paid. There is no negative surprise in the results so far.

Conclusions

I always propagating on focusing on the fundamentals of investing. Good to read analysts’ reports, listen to market talks, including forecasting of macro-economic events, but do not let them dictate too much on your investment decisions. You are well equipped to analyze and make independent judgment on your investment with all the knowledge in fundamental investing that you have already acquired. Make full use of all this knowledge in your investing decision. You should be doing satisfactory in the long run.

I do not see any significant event which will adversely affect the business of Hevea. To me, at RM1.25 now, it is still a steal. Of course it will be fantastic if you can buy at 60 sen. However, sometimes one has to be realistic in our investment, as well as life in general. Don’t you think so? |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-9-2016 01:00 AM

|

显示全部楼层

发表于 23-9-2016 01:00 AM

|

显示全部楼层

| 1. Details of Corporate Proposal | Involve issuance of new type/class of securities ? | No | Types of corporate proposal | Exercise of Warrants | Details of corporate proposal | Conversion of Warrants (HEVEA-WB) | No. of shares issued under this corporate proposal | 5,398,500 | Issue price per share ($$) | Malaysian Ringgit (MYR) 0.2500 | Par Value ($$) | Malaysian Ringgit (MYR) 0.250 | | Latest issued and paid up share capital after the above corporate proposal in the following | Units | 491,473,690 | Currency | Malaysian Ringgit (MYR) 122,868,422.500 | Listing Date | 22 Sep 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 7-10-2016 11:31 PM

|

显示全部楼层

本帖最后由 icy97 于 8-10-2016 04:02 AM 编辑

木板價揚.億維雅派息率高

2016年10月07日

http://www.chinapress.com.my/20161007/木板價揚.派息率高-億維雅價量齊升/

(吉隆坡7日訊)中國碎木板售價處揚升週期,供應緊縮料價格會持續攀升,相信億維雅(HEVEA,5095,主要板工業)可從中受惠,加上派息率看漲。

聯昌證券研究指出,自2015年開始伐木活動抑制使中國面對供應短缺問題,導致進口碎木板需求大漲。這推動碎木板價格按季攀升5%到8%,億維雅從9月開始以雷同漲幅提升價格,有利于賺幅表現。

產量短缺使出口至中國的價格持續提升,估計中國的售價將增5%,提振該公司2017財年每股盈利5.5%。

此外,日圓升值強勁改善日本的購買能力,使億維雅傢具需求強勁。該公司的傢具業務有60%產量供出口至日本,這尚未計算奧運建築帶來的需求增長。

該公司在5月底股東大會中宣布30%派息政策,因此該行將2016至2018財年派息率預測上調至27%到34%之間,相等于每股派息5仙至7.5仙。

該行相信億維雅股價年初至今下滑50%,主要是投資者對出口業缺乏興趣所致。

目前上升週期相信剛開始,該公司在未來6至12個月將由5%到6%的具吸引力收益、碎木板價格攀升、高賺幅甲板需求攀升及日圓和美元升值提振。

同時,該行維持億維雅“增持”評級,合理價為2.02令吉。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 15-10-2016 01:18 AM

|

显示全部楼层

HEVEA(5095) - LATEST News.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 15-10-2016 01:19 AM

|

显示全部楼层

本帖最后由 icy97 于 15-10-2016 01:26 AM 编辑

[分析冷眼大师选股] NO.2 HEVEABOARD BERHAD

Author: GoldenEggs | Publish date: Wed, 21 Sep 2016, 04:18 PM

http://klse.i3investor.com/blogs/Goldeneggs/104806.jsp

今天继续分析第二支冷眼大师大量持有的股,总共持有八百万令吉(包括HEVEA-WB), 其实大师已经在这个公司赚了很多,可能当初投资时成本不到一半,所以说每一支他所投资的股我都会从基本面去学习。

HEVEBOARD 是一家生产particle board 和 ready to assemble products 的工厂,简单来说就是一家板厂。最近几年生意可以说是好得不得了,从2012年净利15.4M到近一年的79.24M (+520%) 的上涨。看到这里大家肯定觉得股票也从0.5飙升到5.08(1 split 4 )。但是从我的估算中,HEVEA仍然是极度被低估,可以说是bursa中排名第三被低估的股票。很大的原因在于管理层被网友抹黑操纵股票。这也让我们有机会买进一支便宜且优质的股票。

好吧,基本面来了。。。PE: 7.30 (对一支成长股来说夸张的低),Dividend Yield 方面就略低了,不到2%但我是觉得既然管理层能善用资金来赚更多钱,那就拿少一点吧。效率方面,29.7% 的Return On Invested Capital (也就是公司一年所赚的钱除以所投入的成本),这很清楚说明了HEVEA 呢是一支非常节省成本且很擅用公司的资金,也可以从这里看得出为什么冷眼大师持有数会比第一篇的SUPERLON多了。

FreeCashFlow/Market Cap 方面呢, 达到了22.6八仙,足足是定存的4倍多,CASH ROIC 更是31.7%。我想你们看到这些数据也不敢相信这是真的吧。HEVEA 目前是一家net cash company (98.76M) 的net cash, 相信风暴来时对公司只是小挑战。这些都是以HEVEA 这一年的盈利计算的,看了以上数据,大家应该明白为什么HEVEA会是第三被低估的股票了。

总结:HEVEA 是一间 NETCASHCOMPANY,非常会擅用资金,效率一流,有野心。我对他的估算在3.02到3.20之间,非常的被低估,你们可以使用你们持有的公司的基本面来比一比就知道了。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 15-10-2016 01:20 AM

|

显示全部楼层

本帖最后由 icy97 于 15-10-2016 01:27 AM 编辑

[分析冷眼大师选股] Heveaboard vs Evergreen

Author: GoldenEggs | Publish date: Thu, 13 Oct 2016, 05:39 PM

http://klse.i3investor.com/blogs/Goldeneggs/106344.jsp

今天要说的就是 Heveaboard 和 Evergreen, 到底投资那一家会比较安全,比较有前途,还有就是比较有价值。

其实,这几天看到 Evergreen 因为美金大起而股价上涨,我非常不解。就算美金上涨,公司长期没有业务发展的话,能赚大钱吗?也许这也是因为大部分投资者没办在股市赚大钱的原因,今天钢铁价起就买钢铁股,明天美金上,就买出口股,跳来跳去,花拳绣腿,能赚大钱吗? 倒不如持有基本面强劲,且有发展的公司,紧握不放,不是更轻松赚钱?

在离我上次发表时 Hevea 的股价从 1.27 上到 1.42,说明了很多人已经开始看到 Hevea 的价值,还有投资风险到底有多低。Paying a dollar for 50 cents, 就是 Hevea, 我很肯定 Hevea 现在的盈利觉对是这个概念。如果盈利下跌或上涨,那就要重新计算。

最好笑就是有些部落客,跟别人说不可以买 GKENT 和 GADANG 因为现在是高价区。。。一间公司是不是在高价区是由价值决定的不是起了100% 就是在高价区。离我上次分享 GKENT 到今天 2.47(23/9) 起到了 2.75。那是不是在高价区? 起了很多了勒!我想说的是,Gkent 的盈利只要一直上,我是会紧抓不放,而且现在离 Gkent 该有的价格还有一段距离,Margin of safety 没有一块买两块那么高了,但是还是可以买的。

我可以跟你说 Gkent 至少值 RM 4.00, 很多股市新手很喜欢看 PE 来决定贵还是便宜,但是我想说如果一家公司高债务,低 PE 你要买?一家公司必须投入非常多的盈利在 Capital expenditure 上面来维持盈利,没有什么 Cash Flow, 你要买? 公司效率普普, 低 PE 就买?

PE 只是反映了公司的盈利和价钱,还有很多其他东西比如说公司的发展,product 的抗竞争的能力我们需要考虑。

说到 Product 的素质,HEVEA 非常努力的努力 move up value chain, 生产更多环保且高素质的 Particleboard, 我们也可以发现,连中国这么竞争的经商环境,HEVEA 也能分一杯羹,说明了这家公司的竞争能力~ 从Profit Margin 不断上升就能看到公司在这方面的努力,比起 HEVEA 的 14%,EVERGREEN 的8%就逊色了。

http://klse.i3investor.com/blogs/Goldeneggs/104806.jsp

从这篇大家可以看一下我分享的HEVEA基本面~

然后现在我们来看 EVERGREEN 的基本面:

债务这几年已经大幅下降,但是还不是一家Net Cash Company,所以这方面 HEVEA 取胜

ROIC:效率方面 12.2%,很大方面在于生产比较便宜,低素质的 Product 所以需要的成本比较高,盈利比较低还有量比较大

Cash Flow:现金流动还是很不错的,不过跟放在 FD 差不多 3.54%。

Revenue 也是几年没有什么起色了~

当了解了 Evergreen 的基本面后,就非常费解,到底这些投机者在做什么?美金起,就想赚快钱。明明就有一家好好的 HEVEA, NET CASH, ROIC:29.7, Cash Flow 在 FD 的五倍?HEVEA 还有一个比较大的优势,就是它小,当一家比较小的公司要增加一倍的价值比起一家大的公司比较容易,而股票翻倍的几率较高。

当看到论坛的投机者还在比较HEVEA 还是 EVERGREEn 比较好时,我心里就在想,怪不得,毕竟股市是一个 zero sum game, 有人赢就一定要有人输。

我崇尚不去预测公司的盈利,单纯看公司的价值,买有减价的公司如 HEVEA,如果盈利下跌,少亏,盈利上升,肯定赚大钱。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 15-11-2016 11:38 AM

|

显示全部楼层

本帖最后由 icy97 于 15-11-2016 08:45 PM 编辑

冷眼推荐股(七):HEVEA

Tuesday, November 15, 2016

http://bblifediary.blogspot.my/2016/11/hevea.html

业务

- 木屑胶合板(Chipboard)

- 木制家具

HEVEA(亿维雅,5095,主板工业产品股),成立于1993年,并于2005年1月12日上市大马交易所主板。

大本营设在森美兰州的HEVEA,其业务主要涉及生产与经销木屑板(Particleboard),除了供应给本地市场外,大部分都出口至其他国家。当中,中国和日本这两国就几乎占了其一半的营业额,其他的国家还包括美国、欧洲国家、印度、阿联酋、东南亚国家、台湾、澳洲等。

此外,该公司也生产一些现成组装(Ready-to-Assemble)木制家具。

其实有常来我部落格的朋友,应该还会记得我曾经介绍过它,那是去年1月的时候,该篇文章为《浅谈HEVEA》。

当时我说这家公司吸引到我的原因是其股价被低估,以及该公司的还债能力非常强。

今天,HEVEA已经完全把银行借贷偿还,并且拥有9800万令吉的净现金。而且在现今充裕的情况下,公司也开始派发更多的股息,相信这是所有股东最希望看到的。

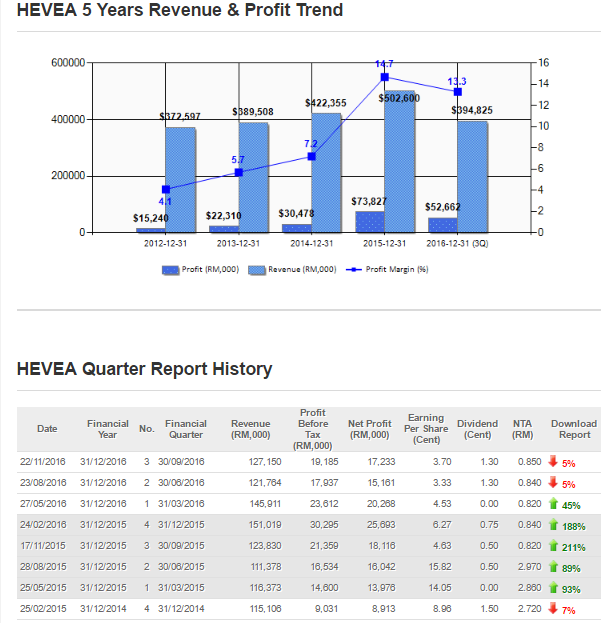

HEVEA的业绩在2015年达到的高峰,营业额5亿260万令吉,净利也达到7383万令吉。

而今年首半年,营业额为2亿6768万令吉,而净利则是3543万令吉。营业额已经已经是去年的一半,然而净利仍然需要再加把劲。

我个人觉得,在公司无需承担贷款利息的压力,以及美元持续升值的这两大因素,HEVEA今年全年业绩应该可以超越去年。

免责声明:

以上投资分析,纯属本人个人意见和观点。

文章所提做出的数据与价格仅供参考,建议大家在买进一家公司的股份前,请先做功课并了解该公司,并衡量应何时进场和离场,任何人因看此文章而造成任何投资损失,本人恕不负责。切记,买卖自负!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 16-11-2016 08:06 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-11-2016 07:31 PM

|

显示全部楼层

本帖最后由 icy97 于 28-11-2016 01:41 AM 编辑

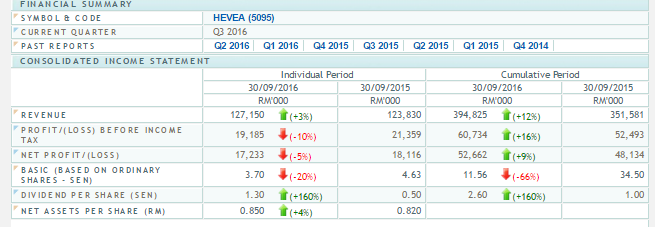

SUMMARY OF KEY FINANCIAL INFORMATION

30 Sep 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Sep 2016 | 30 Sep 2015 | 30 Sep 2016 | 30 Sep 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 127,150 | 123,830 | 394,825 | 351,581 | | 2 | Profit/(loss) before tax | 19,185 | 21,359 | 60,734 | 52,492 | | 3 | Profit/(loss) for the period | 17,233 | 18,116 | 52,662 | 48,134 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 17,233 | 18,116 | 52,662 | 48,134 | | 5 | Basic earnings/(loss) per share (Subunit) | 3.70 | 4.44 | 11.30 | 11.78 | | 6 | Proposed/Declared dividend per share (Subunit) | 1.30 | 0.50 | 2.60 | 1.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.8500 | 0.8400

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-11-2016 08:25 PM

|

显示全部楼层

本帖最后由 icy97 于 28-11-2016 01:41 AM 编辑

【浅谈亿雅】- HEVEA(5095)盈利YOY下滑5%,公司派息1.13仙,PE = 9.56

Tuesday, November 22, 2016

http://harryteo.blogspot.my/2016/11/1379-hevea5095yoy5113pe-956.html

HEVEA是一家充满话题以及受到关注的芙蓉上市公司,去年的涨幅大约290%。股价今年一度暴跌到1.05, 过后又站回了RM1.50以上。今天公司公布了最新一季的业绩,Net Profit YOY下跌了5%,但是17.233 mil的盈利比Q2的15.161 mil进步了13.67%。以2016年前9个月做对比的话,HEVEA的Net Profit按年还是进步了9%。

以下是HEVEA过往几个季度的资产债务表对比,希望对大家有所帮助。

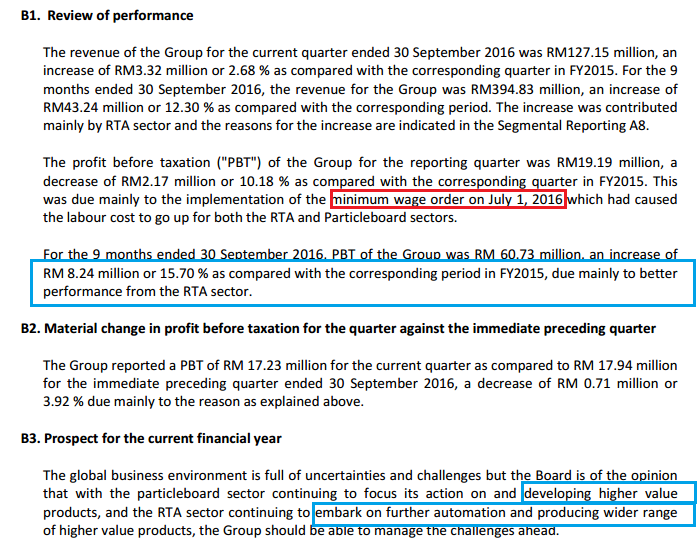

- 营业额YOY上涨了4.42%,但是盈利下滑了5%。主要是因为RTA的Export Tax Incentive已经用完,而且最低薪金制度也拉高了生产的成本。

- Q3的美金季度汇率比Q2高了1%,但是公司却蒙受了大约RM676k的外汇亏损,这有点出乎笔者意料。

- Particleboard的盈利11.37 mil是今年3个季度里最强的一个季度,但是大家仔细看的话,RTA Products的盈利却下滑到7.815 mil。

- 在过去的5个季度,RTA Products每个季度的PBT都保持在10 mil以上,这次盈利的下滑公司却没有在季度报告里有任何的解释。公司只提到全年的营业额以及盈利有所上涨,会继续automate以提高效率。

- CASH IN HAND从下滑到109.79 mil,而债务保持在15.111 mil的水平,net cash = 94.679 mil。现金下滑的其中一个原因是公司提升派息,而且Inventories也增加了2.4 mil左右。

- 不过公司的Gearing - Debt to Equity ratio从0.20下滑到0.17,公司的资产债务表持续在进步着。

公司的Profit Margin因为Tax Incentive减少以及最低薪金而被拉低到13.3%。今年的Q2以及Q3盈利连续两个季度下滑,Q4要雄起才能让公司的盈利保持成长。

公司今年9个月的Net Profit是52.622 mil, 公司下个季度必须要有22 mil的net profit才能保持成长。

假设要保持年度5%的成长,下个季度Net Profit必须有24.86 mil。

假设要保持年度10%的成长,下个季度Net Profit必须有28.61 mil。

保持5%的成长是有可能的,但是要保持10%的成长就必须有历史新高28.61 mil的Net Profit,难度很高。

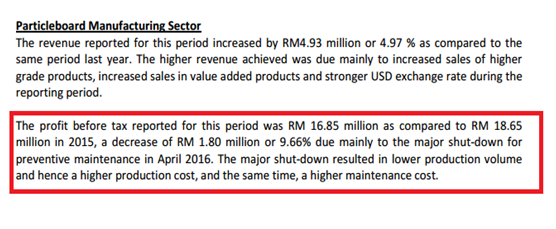

Particleboard盈利减少主要是因为4月major shut down,拉低产量以及增加生产成本,此外也提高了maintenance cost.

总体而言,公司被几个因素所影响着:

- 最低薪金制度导致成本增加

- 虽然RTA Sector在上半年的盈利非常出色,但是在Q3却突然下滑,原因没有写在Quarter Report. 跟失去RTA tax incentive没有关系,因为这些事Profit Before Tax。

- RTA tax incentive已经用完了

总体而言,公司还是努力研发Higher value的产品以及提升机械自动化克服未来的挑战。此外,管理层会善用大笔的cash in hand,明年有可能会进军新的领域以推高公司的成长。

由于2015年公司的盈利上涨了142%,股价也上涨了290%。今年公司的市值已经接近750 mil,所以要保持过去的告诉成长并不容易。公司也醒觉这一点,所以2016派发了更高的股息来回馈股东们。2017年公司必须有更高的盈利成长才能推动股价,因此希望HEVEA的管理层不会让股东们失望。

以上纯属分享,买卖请自负。 |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3092

3092  50

50