|

|

发表于 20-6-2016 11:06 AM

|

显示全部楼层

发表于 20-6-2016 11:06 AM

|

显示全部楼层

本帖最后由 icy97 于 20-6-2016 07:25 PM 编辑

億維雅:高賺幅產品抵銷外匯損失

The Busy Weekly | 2016年06月18日

億維雅董事經理熊豪俊通過電郵對《資匯》表示,全球膠合板今年的供應和需求料穩定,而原料成本增加可能使膠合板價格稍微提高。

同時,熊豪俊說,「我們的出口料將保持穩定,膠合板的需求依然良好,尤其是中國和日本。」

「挑戰方面,我們的產能已難以負荷市場的額外需求,原料成本也在增加。」

那億維雅能否延續去年大好的淨利表現?他回應說,在2015財政年,該公司的60%淨利來自美元兌令吉匯率走強,其餘40%來自較高的賺幅和附加價值產品。

他補充,令吉兌美元今年回揚,固然對億維雅的淨利會有一些影響,但該公司將持續多賣高賺幅產品,抵銷外匯方面的損失。

億維雅在2015財政年第3季(7月至9月)便成為一家淨現金公司,該公司在今年3月也償還了所有以美元計算的貸款,目前可說是無債一身輕。這些貸款是用來增設生產線。

膠合板業務方面,億維雅將專注于生產高檔和更環保的木料產品。

在2016年,億維雅將撥出2000萬令吉的資本開銷( CapEx),以提升該工廠的設施來生產高質量產品。

其中800萬令吉將用來提升膠合板生產線,剩餘的1200萬令吉則將投資在自行組裝(Ready-toAssemble)家具業務,擴大產品組合。

除此之外,億維雅將增設一條名為KREA Kids的生產線,滿足孩童家具市場的需求,

唯一追蹤億維雅的聯昌國際投行分析員預測,億維雅2016財政年的營業額揚升10.03%,至5億5300萬令吉,淨利則上漲15.22%。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 29-6-2016 02:08 AM

|

显示全部楼层

今天排hevea-wb竟然沒中,哭哭..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 18-7-2016 02:25 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 18-7-2016 03:36 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 21-7-2016 07:06 PM

|

显示全部楼层

本帖最后由 icy97 于 21-7-2016 08:22 PM 编辑

Holistic View of HeveaBoard with Fundamental Analysis

Author: Joe Cool | Publish date: Thu, 21 Jul 2016, 12:31 AM

http://klse.i3investor.com/blogs/ivsastockreview/100457.jsp

Background

HeveaBoard and its subsidiaries manufacture, trade and distribute a wide range of particleboard and particleboard-based products. HeveaBoard takes the lead in the manufacturing of particleboard – a reconstituted wood panel derived from rubberwood residues, while its subsidiaries are involved in downstream particleboard based ready-to-assemble furniture manufacturing, trading and distribution of particleboard and wood panel related products.

HeveaBoard was incorporated in 1993 as a private limited company under the name of HeveaBoard Sdn Bhd. The Company was converted into a public limited company in 2004 and assumed its present name, and was subsequently listed on the main board of Bursa Malaysia Securities Berhad in January 2005.

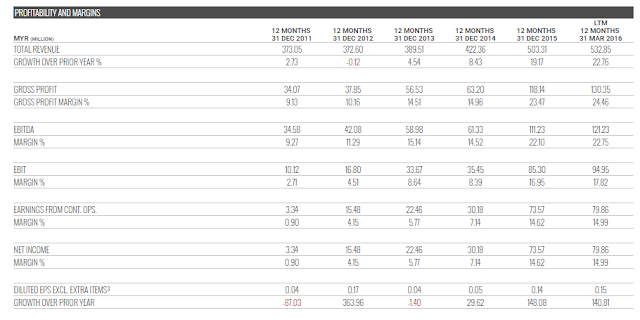

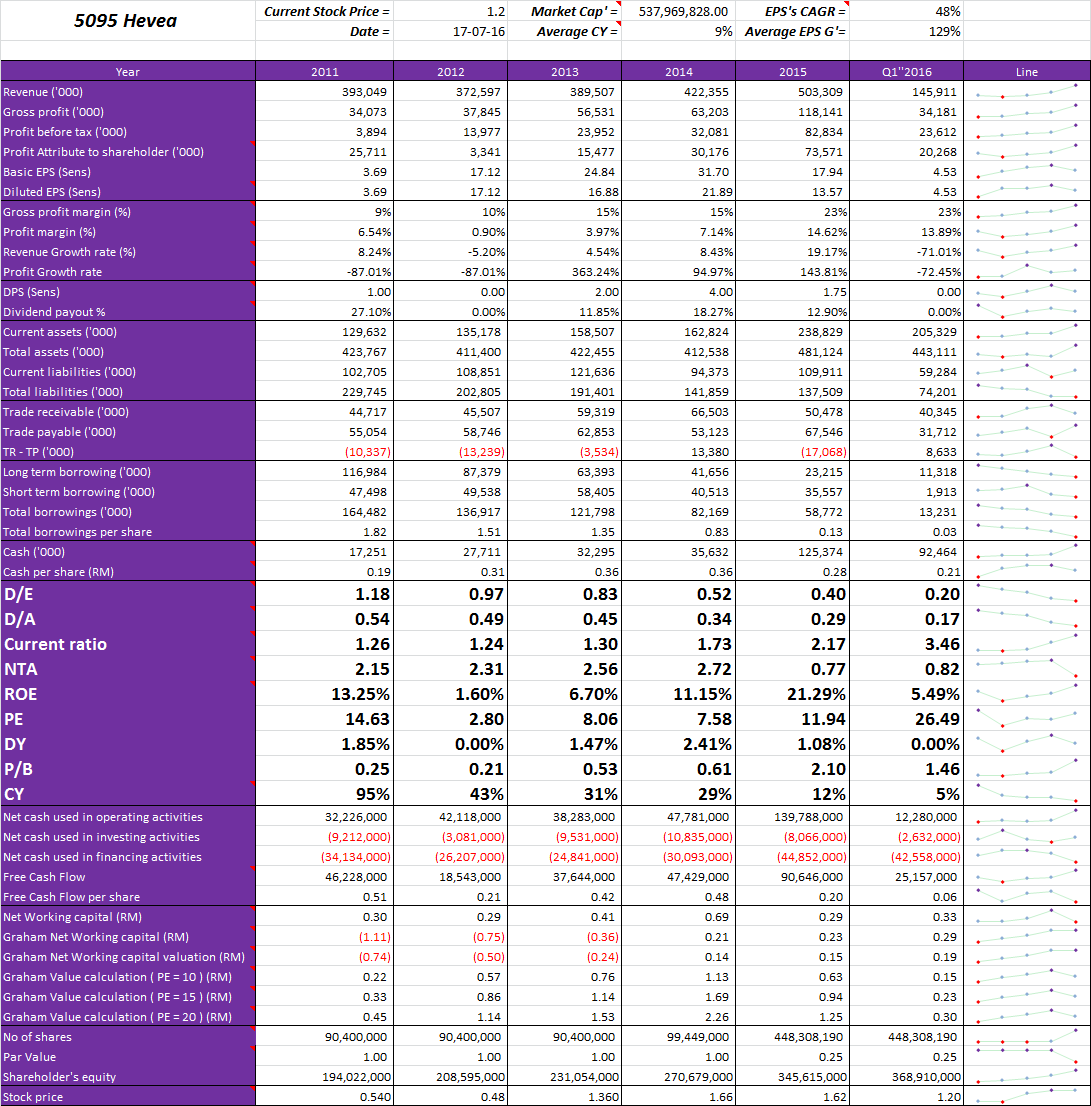

Based on Financial Year (FY) 2015 full year results, HeveaBoard achieved RM 503 million turnover, which is considered to be a mid-size enterprise. Other aspects of the company’s latest financial results are illustrated in the table below.

HeveaBoard (5095.KL) | FY 2015 | TTM (May 2016) | Revenue (RM’000)

| 503,309 | 532,138 | Net Earnings (RM’000)

| 73,571 | 80,119 | Net Profit Margin (%)

| 14.62 | 15.06 | Return of Equity (%)

| 21.16 | 21.72 | Total Debt to Equity Ratio

| 0.17 | 0.04 | Current Ratio

| 2.51 | 3.46 | Cash Ratio

| 1.29 | 1.56 | Dividend Yield (%)

| 2.29 | 2.52 | Earnings Per Share (RM)

| 0.174 | 0.175 | PE Ratio

| 6.92 | 6.86 |

Since FY2011, HeveaBoard’s revenue has been in a growing trend till FY2015 from RM 372 million to RM 503 million per annum. This represents a 35% increase in 5-year period or an average year to year increase of 7.83%.

Net profit wise, HeveaBoard achieved a steeper increasing trend for the same 5-years period from RM 3.3 million to RM 73.8 million, which translates to a 24 times increase in 5 years or average year to year increase of 117%. Having a much higher growth trend in net profit as compared to revenue is one off the most desirable characteristic of a growing company as it shows continuous effective cost management and growing net margin of the company’s product.

Net profit margin wise, HeveaBoard scores a good 14.62% as well as having an excellent Return on Equity at 21.16%.

On company’s debt, HeveaBoard has very low total debt to equity ratio of 0.17, signifies that the company has extremely little borrowings as compared to its shareholder equity value. The company’s current ratio of 2.51 and cash ratio of 1.29 shows a good management on current asset and current liabilities value as well as retaining a good amount of cash and cash equivalent on hand to cater for unexpected events.

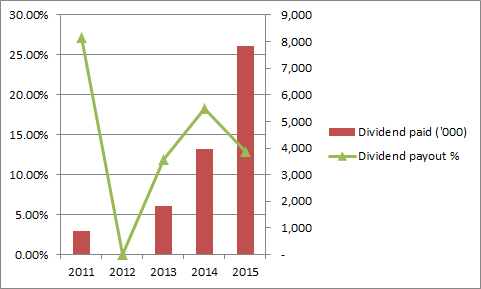

In terms of dividend, HeveaBoard pays an average 2.29% dividend yield, which translates to 1.75 cents per share in FY2015. Although the dividend yield is not high, one notable aspect is that the company’s dividend payout ratio is only at 0.097, which is around 10% of its total net earnings. This indicates that the company retains most of its earnings for debt payment and capital expenditures. Hence, this is resulting in very low debt business model and promising future growths through capital expenditure.

In conclusion, HeveaBoard is a mid-size SME with sound and consistent year to year financial performance. Looking at the Trailing Twelve Months (TTM) financial figures (based on quarterly results till May 2016), HeveaBoard will be continuing its strong financial performance for FY2016 with increasing revenue and net profit. As 93% of HeveaBoard’s revenue are export based, with Japan and China contributing to 54% of its total revenue, any weakening Ringgit will further boost the sales of its products. With its current low PE ratio of 6.92, it is a company that is worth considering as good investment for fundamental investor and the return should be promising.

Next quarterly results announcement should be on the month of Aug 2016 for Q2 results.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 5-8-2016 05:31 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 5-8-2016 08:01 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 23-8-2016 09:12 PM

|

显示全部楼层

本帖最后由 icy97 于 23-8-2016 09:17 PM 编辑

SUMMARY OF KEY FINANCIAL INFORMATION

30 Jun 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Jun 2016 | 30 Jun 2015 | 30 Jun 2016 | 30 Jun 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

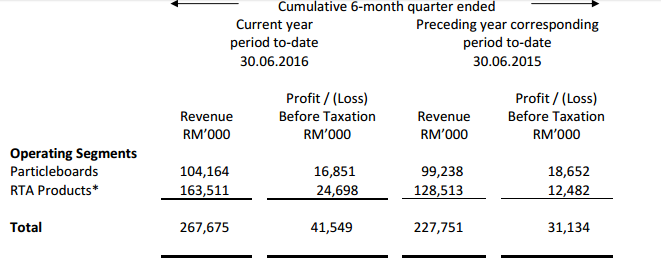

| 1 | Revenue | 121,764 | 111,378 | 267,675 | 227,751 | | 2 | Profit/(loss) before tax | 17,937 | 16,533 | 41,549 | 31,134 | | 3 | Profit/(loss) for the period | 15,161 | 16,042 | 35,429 | 30,019 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 15,161 | 16,042 | 35,429 | 30,019 | | 5 | Basic earnings/(loss) per share (Subunit) | 3.33 | 3.99 | 7.77 | 7.47 | | 6 | Proposed/Declared dividend per share (Subunit) | 1.30 | 0.50 | 1.30 | 0.50 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.8400 | 0.8400 |

| Remarks : | | The comparatives of Basic Earnings Per Share (EPS) and Net Assets Per Share (NA) have been computed/restated to account for the subdivision of every existing one (1) ordinary share of RM1.00 each into four (4) ordinary shares of RM0.25 each (share split) which was completed on 24 July 2015. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-8-2016 09:13 PM

|

显示全部楼层

本帖最后由 icy97 于 23-8-2016 09:20 PM 编辑

HEVEA(5095)盈利YOY下跌5%,,Net Cash暴增到98.46 mil + 派发1.3仙股息!

Tuesday, August 23, 2016

http://harryteo.blogspot.my/2016/08/1329-hevea5095yoy5net-cash9846-mil-13.html

HEVEA(5095)公布了不错的业绩,Net Profit YOY下跌了5%。不少读者应该都在想,为什么盈利下跌笔者还称之为【不错】的业绩?假设大家仔细留意的话,HEVEA的Profit Before Tax(PBT)其实是比去年同期出色的,YOY进步8%。导致Net Profit下滑有两个主要的原因:

- RTA部门的Tax Incentive已经用尽,因此导致Income Tax增加

- 4月的时候工厂关闭维修,因此产量减低。未来两个季度的产 量就会恢复正常。

以下是HEVEA的季度报告分析,希望对大家有帮助。

- 虽然Income Tax增加,HEVEA在Q2的Net profit margin还是可以保持在12.45%的高水平,主要归功于部分产品主攻高端路线拉高毛利率。

- 之前在股动大会跟管理层聊天的时候曾经聊到,工厂shut down维修通常会是在Q1。但是由于今年Q1的订单过多,HEVEA只好把工厂Shut down延迟到Q2.

- 管理层提到工厂在4月shut down大约 8 - 10天,因此Q2的工作日至少减少了10%。这也意味着产量至少下跌10%,而且更高的维修成本也拉低了Q2的盈利。

- 【假设】HEVEA是在Q1 shut down, Q1的盈利YOY还是会继续进步,只是可能涨幅会比较少。那么Q2的产线如常运作的话,Q2的盈利YOY想必是会进步的。

- 不过把两个季度的盈利加起来,FY2016上半年的盈利还是比去年上升了18%.

- 而HEVEA终于摆脱了外汇亏损的拖累,这个季度有2.981 mil的外汇盈利。主要原因是HEVEA几乎清空了美金的债务,手上有大笔的美金资产。而6月30日的美金汇率又比3月31日高了接近2%,因此HEVEA在这个季度有外汇盈利的出现。

- 此外,公司在短短的1年半清还了60 mil的债务,最新的债务只有14.656 mil。

- 而公司手握1.13亿的现金在手,扣除了债务之后的净现金 - Net Cash高达98.46 mil。

- 因此HEVEA已经是不折不扣的【现金奶牛】,也因此派出了历史新高的淡季股息 = 1.3仙。

从上图我们可以看到RTA的营业额比去年增长了许多,反之Particle boards的PBT却在营业进步5%的情况下下滑。

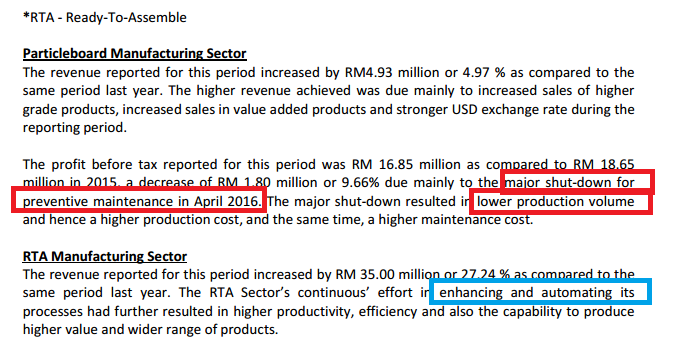

- 公司解释Particle Board产量减低主要是因为major shut-down for preventive maintenance in April 2016. 这也导致了产量下跌以及更高的生产成本,同时维修成本也增加了。

- 而RTA的营业进步27.24%,主要是因为公司极力推广automation以及研发更有价值的产品以提高Profit Margin。

- 相信在未来两个季度Particle Board的产线如常运作,公司的营业额会渐入佳境。

- 公司在RTA的Tax incentive已经用完,因此今年上半年的Income Tax足足比去年多了5 mil。不过Particle Board还有Capital allowance以及Investment Tax Allowance (ITA)的存在,因此可以Offset Taxable statutory income。

- 但是将来这些Tax incentive用完的时候,HEVEA可能会面临FLBHD一样的窘境。因此提高公司的产量以及产品的价值是公司现在的主要任务,这样提高盈利并抵消未来更高的Income Tax。

公司对FY2016的展望:

HEVEA将会研发更加高端有价值的产品以提高Profit Margin,同时也会多元化产品以吸引更多的客户。而且公司在FY2016财政年的派息政策定为30%,较高的派息政策在回馈股东的同时也可以吸引股息投资者的注意。

公司现在的EPS 大约17仙,30%的派息也意味着公司全年必须派发5.1仙或以上的股息。以现在1.18的股价计算,FY2016的周息率超过了4.3%。此外,公司今年将会耗资20 mil在R&D以及Automation,长期来说HEVEA的产能是可以继续成长下去的。

以上纯属分先,买卖自负。

Harryt30

20.30p.m.

2016.08.23

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-8-2016 12:52 AM

|

显示全部楼层

本帖最后由 icy97 于 25-8-2016 01:13 AM 编辑

HEVEA : a broken gem 破碎的宝石

Author: robertl | Publish date: Wed, 24 Aug 2016, 11:49 PM

http://klse.i3investor.com/blogs/heveatimetoalight/102897.jsp

For the past 2 weeks (before yesterday's announcement of Q2 Result), both Hevea and Hevea-WB were under immense selling pressure. Have you ever wonder why such a perceived to be a good stock went through this selling gyrations?

Of course, outside investors like you and me are not priviledged to the inside informations of Hevea. But the tell talle signs were all over the movement of both Hevea and its WB of late.

Learned investors surely know and understand the co-relationship between a mother share and its derivative "son" or the warrant. In all market dynamics, the warrant will always trade at a premium or "out-of-the-money" to its mother shares because of its inherent elasticity. It is this elasticity or leveraging power that attracted investors' enthusiasm, and they are willing to pay a premium for it while at the same time forgoing all dividends that only the mother shares are entitled for.

However, this conventional nature of warrant-premium-over-mother-shares are now broken by Hevea-WB in the last two weeks. As a matter of fact, it still happened today where Hevea shares price closed at $1.16 and WB at $0.895 respectively (conversion ratio 1:1 at a cash tender of RM 0.25 for every new Hevea shares).

Why and what happened?

The answer lies on the non-disclosure to the public on the movement of the shareholdings of the directors and substantial shareholders of Heveaboard Berhad. You may say if that is the case, these interested parties (Directors and Substantial Shareholders of Heveaboard Berhad) may have violated the Bursa Malaysia listing requirements by so doing.

Yes and No, as under the prevailing Bursa Malaysia listing requirements, no disclosure is necessary if it only involves changes in the derivative shareholdings of a listed entity (Hevea-WB in this case). In a plain word, these interested parties need not give a damn to you and me as well as the market regulators to what they do to their Hevea-WB.

This bring us back to why the selling gyration on Hevea and Hevea-WB of late. If you look at the Annual Report 2015 of Heveaboard Berhad, the top two single largest warrant holders of Hevea were both Heveawood Industries Sdn. Bhd. with 32,047,710 and 19,217,240 units repectively or a combined warrant holdings of 42.74% of Hevea-WB.

I have written in the beginning of the year many articles on Heveaboard Berhad and Heveawood Industries Sdn. Bhd. and the shareholders feud in the latter. I can confirm now that all the 42.74% of Hevea-WB have been "disbanded" by Heveawood Industries Sdn. Bhd. and are now gushing out at the gate of Bursa market, ready to be sold off to the public.

This 42.74% or 51,264,950 Hevea-WB selling in the open market for at least the last two weeks explained why the trading volume of Hevea-WB was always bigger than Hevea in this period. When the selling get intensified, the co-relationship between the mother shares and its son come into play, and inadvertantly dragged down Hevea shares price.

Until all these 51,264,950 Hevea-WB finds permanent homes, both Hevea and WB shares price will be under tremendous selling pressure in the medium term. And this has just been aggravated by the not so pleasing Q2 Result of Heveaboard Berhad.

The perceived gem has just been shattered.

PS : I will write again on the 'dark box' of Hevea soon.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-8-2016 03:46 AM

|

显示全部楼层

发表于 25-8-2016 03:46 AM

|

显示全部楼层

EX-date | 06 Sep 2016 | Entitlement date | 08 Sep 2016 | Entitlement time | 04:00 PM | Entitlement subject | First Interim Dividend | Entitlement description | Single-Tier First Interim Dividend of 1.30 sen per ordinary share of RM0.25 each (post-split) in respect of the financial year ending 31 December 2016. | Period of interest payment | to | Financial Year End | 31 Dec 2016 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | BINA MANAGEMENT (M) SDN. BHD.Lot 10, The Highway CentreJalan 51/20546050 Petaling JayaSelangor Darul EhsanTel:03-77843922Fax:03-77841988 | Payment date | 23 Sep 2016 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 08 Sep 2016 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.013 | Par Value | Malaysian Ringgit (MYR) 0.250 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-8-2016 04:07 AM

|

显示全部楼层

| 1. Details of Corporate Proposal | Involve issuance of new type/class of securities ? | No | Types of corporate proposal | Exercise of Warrants | Details of corporate proposal | Conversion of Warrants (HEVEA-WB) | No. of shares issued under this corporate proposal | 7,958,500 | Issue price per share ($$) | Malaysian Ringgit (MYR) 0.2500 | Par Value ($$) | Malaysian Ringgit (MYR) 0.250 | | Latest issued and paid up share capital after the above corporate proposal in the following | Units | 478,136,790 | Currency | Malaysian Ringgit (MYR) 119,534,197.500 | Listing Date | 25 Aug 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 28-8-2016 11:56 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 28-8-2016 02:25 PM

|

显示全部楼层

是指robert仔嗎?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 29-8-2016 02:06 AM

|

显示全部楼层

Name | TENSON HOLDINGS SDN. BHD. | Address | Lot 683, Batu 5

Jalan Kuala Pilah

Seremban

70400 Negeri Sembilan

Malaysia. | Company No. | 34126-V | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary shares of RM0.25 each | Name & address of registered holder | Tenson Holdings Sdn. Bhd.Lot 683, Batu 5Jalan Kuala Pilah70400 SerembanNegeri Sembilan Darul Khusus |

Details of changesCurrency: Malaysian Ringgit (MYR) | Type of transaction | Description of Others | Date of change | No of securities

| Price Transacted ($$)

| | Others | Exercise of warrants | 23 Aug 2016 | 6,300,000

| 0.250

|

Circumstances by reason of which change has occurred | Conversion of 6,300,000 Hevea Warrants B by Tenson Holdings Sdn. Bhd. | Nature of interest | Direct | Direct (units) | 6,300,000 | Direct (%) | 1.32 | Indirect/deemed interest (units) | 154,241,890 | Indirect/deemed interest (%) | 32.28 | Total no of securities after change | 160,541,890 | Date of notice | 26 Aug 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 29-8-2016 11:19 AM

|

显示全部楼层

本帖最后由 icy97 于 29-8-2016 03:04 PM 编辑

Hevea- A broken Gem is still a Gem

Author: TopShare | Publish date: Thu, 25 Aug 2016, 08:20 PM

http://klse.i3investor.com/blogs/topshare94.blogspot.my//102987.jsp

First of all, I would like to thank a " Blogger " for bringing Hevea to spotlight again. Hevea has been trading boringly last few months. I am glad that they have brought some excitement to Hevea again.

I don't really know the truth of the allegation that made by Robert since I am not an insider. So, my evaluation of Hevea is solely based on the financial report and I still believe that Hevea is a good company and worth the risks.

Here is my reasons:

1 ) Despite all the allegations made by the " Blogger ", the performance of Hevea is still quite satisfactory judging from the latest two quater reports. Nothing really bad as proclaimed by the " Blogger " has happened. Company has turn to a net cash company and profit and margin is good. Cash flow is good too.

2) Director has fulfilled his promise of rewarding shareholder. As promise in the AGM, director has started to pay dividen ( around 2.2% ) in two consecutive quater report. For me, I would say that he is the man of his word and trustworthy in my humble opinion.

3 ) I don't see any big problem in the latest report. Indeed, the profit has dropped 6% but it is mainly due to the shut down of operation and higher tax which don't really affect the fundamental of company. Besides, It has performed better than its peers such as evergreen and flbhd.

4 ) Hevea's prospect is still good. Tokyo Olympic is coming soon and Japan is the biggest custumer for Hevea. Ringgit is stable at RM 4. Company still focus on high quality product and it is popular in China. Everything seems fine for me.

Conclusion, I would like give my 2sens to those who are still holding keep calm and relax lah. We don't know what proclaimed by the " Blogger " is true or not but judging from the report, it is doing fine!! Ignore all the noises and believe in yourself and have faith. Let's walk through to this storm together!! Cheers !! Have a great day everyone!!

|

|

|

|

|

|

|

|

|

|

|

|

发表于 30-8-2016 04:55 PM

|

显示全部楼层

|

家私股大地震.. |

|

|

|

|

|

|

|

|

|

|

|

发表于 30-8-2016 06:21 PM

|

显示全部楼层

Hevea : ALERT .. breaking STRONG support. SELL.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 30-8-2016 06:23 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 30-8-2016 11:15 PM

|

显示全部楼层

本帖最后由 icy97 于 30-8-2016 11:48 PM 编辑

【亿雅风暴】- HEVEA(5095)真的有那么差吗??

Tuesday, August 30, 2016

http://harryteo.blogspot.my/2016/08/1342-hevea5095.html

5月30日笔者出席了HEVEA(5095)在芙蓉的股东大会,当时公司宣布了30%的派息政策。股东大会之后跟管理层聊天,当时他们说Q2的4月Shut Down了一阵子维修机器。通常Shut Down都是在Q1,因此大家可以注意到过往的Q1都是全年最差的季度。延迟Shut Down的原因是因为Q1的订单过多,因此4月Shut Down导致YOY的盈利下滑了5%。

不过公司遵守了自己的诺言,Q2派发了1.3仙的股息,这也是HEVEA上市以来派发最高的一次单季股息。这几天股市开始回调,很多中小型股下跌5 - 10%不等。不过HEVEA的跌幅有点夸张,股价从8月22日的1.19, 短短下跌到现在的RM1.05, 跌幅11.76%,直逼1年新低。全年盈利下滑不到1.5%,股价却下跌了接近12%,这到底是为什么呢?

上图是HEVEA过往10个月的股价走势,1月5日的时候突破闭市新高RM1.73,隔天一度走高到RM1.79。因为美金走低以及Mr Robert的文章出现,HEVEA的股价在双重打击下一直插水到RM1.15。虽然有几次尝试反弹,但是始终无功而返。而RM1.18也成为了这8个月来最强的Support,只要跌破了RM1.18,几天之内一定会反弹回来。

但是这个星期HEVEA的成交量暴涨,今天更是来到4个多月的顶峰 - 6.403 mil股,卖压非常强劲,RM1.18的支撑也在上个星期失守。卖压强劲原因如下:

- 盈利下滑5%,部分的散户感到失望并丢货。

- 市场开始回调,大部分的中小型股都都中招,投资者套利

- Mr Robert的文章再度出击,部分散户感到恐慌丢票。

不过假设仔细研究的话,为什么这么多的价值投资者还是那么推崇HEVEA,还是对HEVEA保持着信心呢??

- 公司的现金流不断进步,手握113.116 mil的现金,拥有98.46 mil的Net Cash。一个季度的现金流几乎增长了20 mil之多。

- 提高派息政策,FY2016已经派发了2.3仙的股息,全年周息率介于4.5 - 5.0%之间。

- 拨出RM 20 mil的CAPEX研发产品以及提高产能,长期可以振兴业务的成长。

- 公司的营业额以及盈利连续4年保持成长,可见管理层能力有多么出色。

对于Mr Robert所说的一切,身为散户的我们无从得知真假。希望管理层可以站出来让这场闹剧可以尽早结束,也避免无辜的小股东的利益受到伤害。

或许来个大调整,股价可能会再度像去年8月下跌到83仙。HEVEA真的有那么差吗??每位投资者心中都有一把尺,假设把一家公司比喻成一件货物,每个人给它的【标价】都会不一样。

不要碰你不了解的公司,因为你不知道它在做什么。

不要尝试投机取巧,因为历史证明90%的人都失败了。

共勉之。

以上纯属分享,买卖自负。

Harryt30

21.00p.m.

2016.08.30

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3267

3267  68

68