|

|

【PAVREIT 5212 交流专区】柏威年产托

[复制链接]

[复制链接]

|

|

|

发表于 25-11-2011 11:44 AM

|

显示全部楼层

发表于 25-11-2011 11:44 AM

|

显示全部楼层

回复 160# 独孤球拍

之前是rm0.08 买进的咯。。然后卖了,又在买,又在卖。咯。哈哈 |

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 12:36 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 02:05 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 03:10 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 04:01 PM

|

显示全部楼层

回复 162# 独孤球拍

要是赚我会在那边诉苦咩。我是买到2.1的那时候咯。还在放。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 05:07 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 09:22 PM

|

显示全部楼层

各位 !我要宣布一件事。。。我衰咗 !

piratesinvestor 发表于 24-11-2011 05:53 PM

+1...我都衰咗 ! |

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 11:08 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 25-11-2011 11:19 PM

|

显示全部楼层

第一次申请就衰咗.gif) .gif) |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 01:04 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 26-11-2011 01:26 AM

|

显示全部楼层

拜托,等我在 Open Market 买了之后再起吧。。。不要起的太快啊,拜托拜托。。。 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 26-11-2011 01:28 AM

|

显示全部楼层

Gas Malaysia 又延迟了。。。神啊 !救救我吧!请让我买了 Pavilion Reit 之后才起啊  |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 10:05 AM

|

显示全部楼层

拜托,等我在 Open Market 买了之后再起吧。。。不要起的太快啊,拜托拜托。。。

piratesinvestor 发表于 26-11-2011 01:26 AM

好好好。。。不卖PavReit也不会有钱买Gas Malaysia... |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 02:28 PM

|

显示全部楼层

我也要插一脚。。等一等别起太快 |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 06:49 PM

|

显示全部楼层

平均RM16。76 psf

rental rate 是97。9%

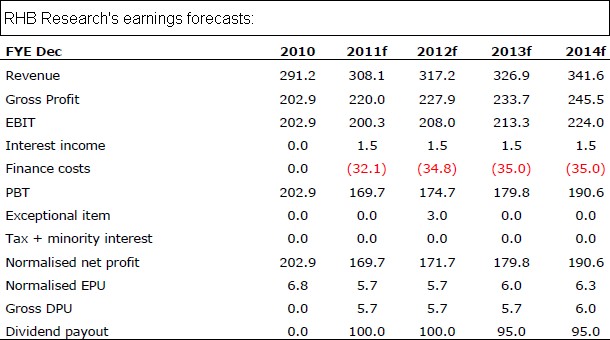

Are you bored of the current small market capitalization of REITs in Malaysia? I think Sunway REIT (the largest REIT right now) is by far sitting there very lonely without anyone closer to it. Come 7th December 2011, we will witnessed a new contender - Pavilion REIT, to challenge the title. Although it may started-off in 2nd place, the new REIT may grows to clinch the first place from SunREIT. Below is some info taken from RHB Research report on the IPO;

Pavilion REIT (PavREIT) has an asset size of RM3.5bn, just after the largest MREIT - Sunway REIT’s RM4.5bn. PavREIT has two assets – Pavilion KL Mall which is worth RM3.4bn and Pavilion Tower (office) RM128m.

The Prime Asset

Pavilion Mall is one of the only four premium retail malls in KL. It is designed to complement the malls along Jalan Bukit Bintang, developing the street to a key shopping destination in the region. Located at the “Golden Triangle”, which is the business, shopping, entertainment and tourism district, the mall enjoys massive catchment of population. It has an NLA of 1.33m sqf.

Since it commenced its operations in late 2007, occupancy has consistently stayed above 96%, with a 3-year CAGR of 4% in average rental rate. With such a short operating history, the mall has recorded 31m visits in 2010, comparable to Suria KLCC’s 40m footfalls. Over the longer term, Pavilion Mall is poised to enjoy higher number of visits as it will sit near to the upcoming MRT station, which is less than 300m away. The covered skybridge currently under construction that connects Pavilion Mall and KL Convention Centre which in turn adjoins Suria KLCC and the Petronas Twin Towers, will also pull in more shopper traffic between the two tourist spots.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 06:53 PM

|

显示全部楼层

不过fair vaue 是RM1.14

快快第一天就进场,手快有,手慢就没有了!

The Pavilion Tower (NLA of 167k sqf) is an office tower connected to Pavilion Mall. It currently has an occupancy rate of 41.4% (expected to achieve 80% by year end), housing Malton roup, Mrail International, Clever Eagle and Aker Engineering (from 1st July). As the office tower only contributes about 2% to total rental income, coupled with the oversupply of office space in KL city centre, we are neutral on this commercial asset.

Future Growth Potential

Three other retail assets can potentially be injected in future for growth. PavREIT has been granted rights of first refusals (ROFR) by its sponsor and a 3rd party to purchase fahrenheit88, Pavilion Mall extension and an upcoming community mall in USJ Subang. These assets are estimated to have a combined value of about RM1.5-2bn. We believe the injection of assets will take 2-3 years, as only farenheit88 is still in the early stage of operation, and the other two malls will only be completed in three years’ time.

How to Value?

We benchmark PavREIT against KLCCP. Although KLCCP includes non-retail assets such as office towers and hotel apart from Suria KLCC, all these assets are of Grade A class. To reflect its prime status, we value PavREIT at a target yield of 5%, which is close to the average yield of 4.72% for KLCCP over the past 5 years (we gross up to exclude the impact of corporate tax – as REITs do not have corporate tax component). This translates to a fair value of RM1.14, based on our FY12 DPU estimate |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 07:39 PM

|

显示全部楼层

为何我的 maybank 2u 还在 pending 的?

Status EnquiryView the status of your share applications Issuing HouseShare Issue NoShare NameUnits AppliedAmountChannelStatusReimburse AmountPartial/Successful Amount

MIHH0524PAVILION REAL ESTATE INVST TRUST4000RM3,520.00M2UPendingRM0.00RM0.00 |

|

|

|

|

|

|

|

|

|

|

|

发表于 26-11-2011 10:39 PM

|

显示全部楼层

为何我的 maybank 2u 还在 pending 的?

Status EnquiryView the status of your share applications

penangbjboy 发表于 26-11-2011 07:39 PM

没有消息,就是好消息  |

|

|

|

|

|

|

|

|

|

|

|

发表于 27-11-2011 08:36 AM

|

显示全部楼层

hwang DBS 的 FAIR VALUE 只有 RM1.00 nya

Pavilion REIT (Offer price 88 sen)

Fair value of RM1: Pavilion REIT will be the sole premium retail REIT in Malaysia upon listing, with its most valuable asset being Pavilion KL Mall (with 1.3 million sq ft of net lettable area [NLA]), which is valued at RM3.4 billion. The REIT also manages Pavilion Tower — a 20-storey office tower with 167,400 sq ft of NLA valued at RM128 million. Pavilion KL Mall has a diversified tenant base, ranging from supermarkets/department stores (Parkson, Mercato) to high-end fashion outlets (Prada, Gucci, Michael Kors) only available in one or two malls in Malaysia. Overall occupancy rate is 99% with average rental rates of RM16.76 per sq ft (retail) and RM5.92psf (office).

Near-term growth will be organic, driven by positive rental reversions on expiring leases. Some 67.2% of Pavilion KL Mall's leases are due to expire in FY13, which would lift our FY13F revenue forecast by 4% year-on-year (assuming 5% rental rate hike) to RM324.7 million. Y-o-y growth for FY12 is expected to be marginal as only 5.5% of the mall's occupied NLA is set for renewal. We understand the managers are actively searching for yield accretive acquisitions in the Klang Valley, Penang and Johor that fit the REIT's profile. Pavilion REIT also possesses rights of first refusal (ROFR) for Pavilion KL Mall extension and a retail mall in USJ Subang Jaya. Pavilion REIT also has ROFR for fahrenheit88, a 300,000 sq ft NLA mall located nearby, with plans to inject it into the REIT as early as 2014.

Pavilion REIT — which would be using 93% of its gross IPO proceeds of RM695 million to part finance the purchase price of RM3.3 billion — would have a gearing of 20.1% post-listing, below the 50% gearing limit. This suggests it could borrow an additional RM1 billion to fund its future acquisitions.

Our RM1 fair value is based on a discounted cash flow analysis with 7.5% weighted average cost of capital, 3% terminal growth and 0.5 Beta (based on CapitaMalls Malaysia Trust), thus valuing Pavilion REIT at a market capitalisation of RM3 billion. At our target price of RM1, the stock offers a distribution yield of 5.8% (based on FY12F dividend per unit of 5.8 sen). This is broadly comparable with the one-year forward yields for Sunway REIT (5.7%) and CapitaMalls Malaysia Trust (6.1%), its closest peers with dominant retail exposure and market capitalisation. — HwangDBS Vickers Research, |

|

|

|

|

|

|

|

|

|

|

|

发表于 27-11-2011 08:42 AM

|

显示全部楼层

KENANGA 的 FAIR VALUE 只有 RM1.12

Analysis: Pavilion REIT seen as a good defensive investment

HIGHER MARKET CAPITALISATION: As 96 per cent of its appraised property value of RM3.54 billion is from Pavilion KL Mall, Pavilion REIT offers the largest exposure to the retail sector of any Malaysian REIT by appraised value, says Kenanga Investment.

KUCHING: Pavilion Real Estate Investment Trust (Pavilion REIT) is seen as a good defensive investment as its future yields are expected to steady under current volatile market conditions.

Comprising Pavilion Kuala Lumpur Mall (Pavilion KL), with 1.34 million square feet (sq ft) of net lettable area (NLA) and Pavilion Tower (0.17 million sq ft NLA), the REIT’s mall and office spaces were 98-per cent and 41-per cent occupied, respectively.

With an initial market capitalisation of RM2.64 billion (based on three billion units in issue based on an indicative initial public offering, or IPO, retail price of RM0.88 per share), Pavilion REIT would be the second largest behind Sunway REIT, which has a market capitalisation of RM3.1 billion.

Kenanga Investment Bank Bhd (Kenanga Investment) stated in a research note, “As 96 per cent of its appraised property value of RM3.54 billion is from Pavilion KL Mall, Pavilion REIT offers the largest exposure to the retail sector of any Malaysian REIT by appraised value.

“The group intends to have a 100-per cent payout policy of its distributable income. We have assumed the mall will have 100 per cent occupancy for financial year 2011 (FY11) and FY12 estimated, while the office will be 82 per cent and 100 per cent occupied, respectively, for the two years.

“We expect financial year 2011 FY11-12E net profit of RM163 million to RM167 million, and a gross dividend per share of 5.6 sen to 5.7 sen (6.4 per cent to 6.5 per cent yield) based on 100 per cent payout of the profit after tax.”

Assuming the stock would trade at its book value of RM0.94 per unit, the group could raise RM564 million in funds and increase its market capitalisation by 20 per cent, Kenanga Investment opined.

Based on annualised actual first half of 2011 combined mall and office income, the group had achieved gross property yields of 8.7 per cent, which Kenanga Investment believed was ‘extremely commendable’ against retail space cap rates of 6.5 per cent to 7.5 per cent.

It also pointed out the management’s ability to pick the right tenant mix and ensure strong rental accretions, adding that the risk of oversupply of rental rates was minimal as it would be unlikely in Kuala Lumpur’s ‘Golden Triangle’.

Kenanga Investment valued the Pavilion REIT at RM1.12 – based on the Gordon Growth Model – with 7.6 per cent required rate of return, three per cent terminal growth, FY12 estimated net dividend per unit of 5.2 sen, implying a forward price to book value of 1.2 times.

Read more: http://www.theborneopost.com/2011/11/16/analysis-pavilion-reit-seen-as-a-good-defensive-investment/#ixzz1ev9FaCkS |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

.gif) 怎么讲到好像亏的

怎么讲到好像亏的  勇气可嘉,佩服佩服 !

勇气可嘉,佩服佩服 !

3063

3063  63

63