|

|

发表于 7-9-2016 02:01 PM

|

显示全部楼层

发表于 7-9-2016 02:01 PM

|

显示全部楼层

本帖最后由 icy97 于 7-9-2016 08:31 PM 编辑

工业4.0新革命的高科技战略计划,这又和大马股市的PENTA有何关系?

2016年9月6日星期二

http://life1nvest.blogspot.my/2016/09/40penta.html

工业4.0是德国政府提出的一个高科技战略计划。该项目由德国联邦教育局及研究部和联邦经济技术部联合资助,投资预计达2亿欧元。旨在提升制造业的智能化水平,建立具有适应性、资源效率及人因工程学的智慧工厂,在商业流程及价值流程中整合客户及商业伙伴。其技术基础是网络实体系统及物联网。

2014年11月李克强总理访问德国期间,中德双方发表了《中德合作行动纲要:共塑创新》,宣布两国将开展工业4.0合作,该领域的合作有望成为中德未来产业合作的新方向。而借鉴德国工业4.0计划,是“中国制造2025”的既定方略。

另外日本失落了十年之久,目前安倍也将展开4.0工业革命来帮助经济走上复苏的道路。

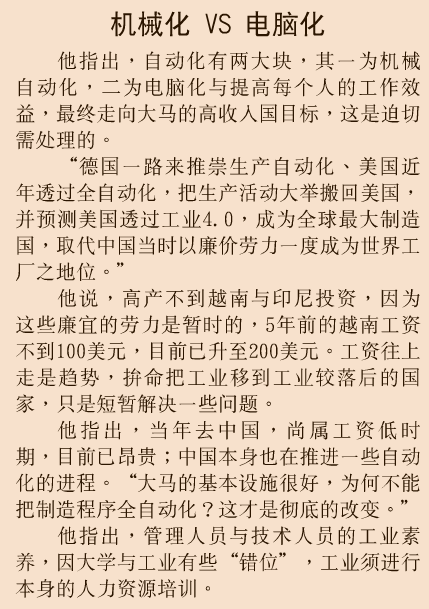

自动化抢走饭碗.亚洲血汗工厂将走入历史亚洲“血汗工厂”的形象即将走入历史,主要是被科技取代。(美国.纽约6日讯)亚洲“血汗工厂”的形象即将走入历史,主要是被科技取代。据国际劳工组织(ILO)公布的报告指出,东南亚约920万纺织与制鞋业的劳工中,有近三分之二正面临自动化的威胁。其中柬埔寨劳工的被取代率将达88%,越南86%,印尼为64%。这种转变以柬埔寨最明确。从1990年代中期以来,全球纺织及制鞋业相继将工厂移入柬埔寨,2015年两项行业的出口额达63亿美元,占出口收入约80%,劳工雇用数达63万人,且2014至2015年平均月薪提高到175美元。中国、越南的成衣制造中心情况亦然。但好景不再。来自其他低工资国家的竞争,持续压低全球成衣价格,2006至2015年间柬埔寨输美成衣售价下跌24%,加上工资上升,使业者面临危机。若不关厂,只能加强动化生产能力。这仅仅只是开始。3D列印及其他新兴科技将使业者能以高度的品质提供客制化的产品,生产速度远超过血汗工厂。更严重的,则是一些西方企业可以在国内采用同样的客制化新科技,完全停止将工厂移往海外。好消息则是亚洲的工厂落实自动化后,可以为本地的消费者服务,尤其是中国,而且各国未来的服装及鞋类需求量也将增加。

坏消息则是各国很难为这些失业的劳工创造新的就业机会。文章来源:星洲日报‧财经‧2016.09.06

以上都是工业4.0的宏观点评。

国内点评-4.0工业的明星股-PENTA 国内点评-4.0工业的明星股-PENTA

PENTA-是一家在槟城的投资控股公司,拥有两项核心业务,分别是制造自动化设备器材(AUTOMATED EQUIPMENT)和自动化生产解决方案(AUTOMATED MANUFACTURING SOLUTIONS),在2015年进军新的业务-智能家居解决方案系统。按2016首季度业绩来看,占整体营业额的贡献比重,分别是制造自动化设备器材75%,自动化生产解决方案23%和智能家居解决方案系统2%。

PENTA的展望

以下的图片显示PENTA的技术是符合工业4.0的水准,所以能够受惠于工业4.0的大趋势。

-Source from PENTA annual report

国内政府呼吁厂家机械化以及减少对人力的依赖

从今年7月1日开始马来西亚政府提高最低薪金制,西马半岛的最低薪金制从每月900令吉提升至1000令吉,东马则从800令吉提高至920令吉。随着最低薪金制和人头税大幅的调涨使得我国人力资源成本高涨。政府认为目前调涨外劳人头税合理,不会影响国内经济运行,也有助于业主实施自动机械化,实现减少依赖外劳的目标。政府呼吁厂家以机械代替人手,这将会刺激PENTA的机械化产品销量走高。

PENTA管理层指出手套制造业已经正在改革进行机械化,是FY 2015

大部分的营业额的重点来源。未来手套制造业的机械化需求趋势将会继续增长以及贡献于FY 2016。

手套制造业有话要说

近期KOSSAN管理层也在报章上透露自动化是成长的关键。以下图片原文是来自KOSSAN管理层。

另外,PENTA的年报透露自动化设备器材供不应求

由于需求大增,公司计划着使目前的生产产能翻一倍。

PENTA的新业务-智能家居

国外相同概念的智能家居影片介绍

智能家居拥有庞大的增长潜能?

automation solution for a smarter home

以下是PENTA管理层对此行业潜能的看法

“The Building Services Research and Information Association (BSRIA) report says that in Asia, the smart building market is projected to grow from US$427bil (RM1,580bil) to US$1,036bil in 2020, creating vast opportunities for advance building technologies and services. “

China, for example, is building 36 smart cities, one of which is a 250 billion yuan low carbon model city in Tianjin.

“Songdo IDB and Fujisawa are two smart cities under development in South Korea and Japan.

“Singapore will become a smart nation by 2015 and Iskandar is the flagship smart city in Malaysia, while Delhi Mumbai Industrial Corridor will be the smart city of India,” he says.

基于管理层看好智能家居市场拥有庞大潜能所以进军这个新业务。

去年PENTA以578万令吉,收购大马Origo Ventures全数股权。

Origo Ventures是一家产业管理公司,拥有超过14年经验。

主要客户包括双威(SUNWAY,5211,主板产业股)、TRC协作(TRC,5054,主板建筑股)、打南(TALAM)和IOI产业(IOIPG,5249,主板产业股)。

腾达科技指出,该公司要进军智能家居和建筑物方案市场,收购Origo Ventures是更有效和低风险的做法。

该公司认为,智能家居和建筑物方案市场拥有庞大潜能。完成这项收购活动后,将有更多管道推广智能家居和建筑物方案。

此外,腾达科技也相信,将从OrigoVentures现有的产业管理合约中受惠。

管理层透露:预计今年FY 2016 Origo Ventures能为公司的盈利贡献10%对比去年只有5%,而在未来5年能提高至30%。

业绩展望

2016年第二季度业绩显示营业额,净利和EPS一同再创单季度业绩的历史新高,所以股价随着突破历史新高也合情合理。

资产负债表

PENTA是一间没有短/长期债务的企业,属于净现金公司,每股净现金高达RM 0.1049。

估值

2012-2015年,PENTA 的Gross profit CAGR高达25.8%。

2012-2015年,PENTA 的Net profit CAGR高达57.7%,已扣除了2015年第三季度RM 2.6 million的一次性盈利。

目前PENTA的PE低于10倍,在一个双位数的成长公司是属于偏低的。

管理层有话要说

以下是管理层对未来展望的信心喊话,管理层不担心目前经济的状况,公司的行业将持续增长,PENTA是个技术门槛高以及高附加值的生意模式,并且能够提供完整智能生态系统。

Pentamaster’s optimism about its outlook, regardless of the current global and domestic economic slowdowns, stems from the fact that its business strategy focuses on providing a complete ecosystem of automated products and testing solutions.

“Most people said recession could happen in 2016, but I do not see it in the value-added semiconductor sector. We are involved in smart devices such as microphones, light sensors, pressure sensors, and MEMS gyros (a sensor put into smart devices), on top of automation handlers.

“We provide the complete ecosystem, meaning the handling plus testing. We write test programmes by understanding their products. There is no cost involved. Our customer base is of the high-end value-added tier, where they want the total ecosystem. Hence, our profit margin has grown. We used to sell machines for RM300,000, but now we can sell for more than RM1 million,” he said.

三十大股东一览

大马投资大师-冷眼也是此股的大股东之一

总结:

- 受惠于工业4.0的大趋势

- 大马政府执行新措施刺激与呼吁厂家机械化,最低薪金制和人头税大幅的调涨使得我国人力资源成本高涨

- PENTA的新业务-智能家居庞大的增长潜能

- PENTA是个技术门槛高以及高附加值的生意模式,并且能够提供一条龙整个智能生态系统

- 2016年第二季度的营业额将会创单季度业绩的历史新高,所以股价随着突破历史新高也合情合理

- 属于净现金公司,每股净现金高达RM 0.1049

- 大马价值投资大师-冷眼也是此股的大股东之一

- 由于需求大增公司计划着使目前的产能翻一倍

- 目前PENTA的PE低于10倍,在一个双位数的成长公司是属于偏低的

|

|

|

|

|

|

|

|

|

|

|

|

发表于 25-9-2016 04:36 PM

|

显示全部楼层

发表于 25-9-2016 04:36 PM

|

显示全部楼层

Notice of Interest Sub. S-hldr (29A)| PENTAMASTER CORPORATION BERHAD |

Particulars of Substantial Securities HolderName | PHEIM ASSET MANAGEMENT SDN. BHD. | Address | 4th Floor, UBN Tower,

Jalan P. Ramlee

Kuala Lumpur

50250 Wilayah Persekutuan

Malaysia. | Company No. | 269564-A | Nationality/Country of incorporation | Malaysia | Descriptions (Class & nominal value) | Ordinary shares of RM0.50 each | Name & address of registered holder | PHEIM ASSET MANAGEMENT SDN. BHD.4th Floor, UBN Tower, Jalan P. Ramlee, 50250 Kuala Lumpur. |

| Date interest acquired & no of securities acquired | Currency | Malaysian Ringgit (MYR) | Date interest acquired | 27 Jun 2016 | No of securities | 7,567,083 | Circumstances by reason of which Securities Holder has interest | Pheim Asset Management Sdn. Bhd. has interest in total of 7,567,083 shares of Pentamaster Corporation Berhad | Nature of interest | Direct | Price Transacted ($$) |

|

| | Total no of securities after change | Direct (units) | 7,567,083 | Direct (%) | 5.163 | Indirect/deemed interest (units) |

| | Indirect/deemed interest (%) |

| | Date of notice | 22 Sep 2016 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 26-9-2016 08:55 PM

|

显示全部楼层

本帖最后由 icy97 于 26-9-2016 11:03 PM 编辑

腾达科技 PENTAMASTER – 分享投资过程

Author: RicheHo | Publish date: Sat, 6 Aug 2016, 10:53 PM

http://klse.i3investor.com/blogs/rhinvest/101572.jsp

PENTA是一家在槟城的投资控股公司,主要提供综合创新服务,包括自动化和半自动化生产机械和配备、设计和生产精密机械部件,以及设计、装配和安装电脑化的系统和设备。简短来说,他提供先进的科技方案与服务,以协助客户在各自的工业领域精益求精、应付生产挑战及维持竞争力。

早在2013-2014年,PENTA非常依赖于电子和半导体领域,当时这领域的贡献是60-70%。因此,这领域的淡季将直接影响PENTA所供应的测试处理设备和自动化设备的需求。基于半导体领域过于波动,PENTA在2015年采取了多元化策略至具有抗跌力的手套、医疗器材、流动设备、汽车和LED领域,并逐渐减少对半导体业务的依赖。

在2015年3月,PENTA在BATU KAWAN工业区以RM5.02m,购买了一块面积达3.23英亩的土地。根据PENTA的通告,由于生产活动增加,公司需要更大的空间作为产品组装与测试地点。目前,PENTA的建筑工程依然还没完成。一旦完成后,PENTA预计在未来几年,会100%全面提升产能!这对于PENTA的股东来说是值得兴奋的。

在2015年7月,为了改善业务表现,PENTA脱售了旗下2家子公司,【PENTAMASTER ENGINEERING】 和【PENTAMASTER SOLUTIONS】。当时,这2家公司已经连续亏损了好几年,并直接拖累PENTA的财务表现。这2家公司在FY14的总合亏损高达RM3.24m!因此,脱售完成后,PENTA在接下来的业绩全面提升。

在2015年9月,PENTA以RM5.78m收购了【ORIGO VENTURES】100%的股权。这家公司是主要涉及产业管理,并拥有超过14年经验。当时,PENTA主要是想借【ORIGO】的产业管理管道,进军智能家居和建筑物方案市场。简短来说,这个智能家居科技可以让一家人更舒服的过生活。他们只需要一部智能手机在手,就能遥控家里的电视、保安系统、音响、冷气等等。此外,【ORIGO】当时手上还握有RM3m的订单。因此,笔者认为这业务非常有庞大潜能,收购肯定会对PENTA有利无弊。

日前,PENTA FY16Q2的业绩已经出炉了。PENTA的盈利相比去年同个季度和上个季度双双进步了超过100%! 它的3个业务自收购【ORIGO】以来,终于同步做出了正面的贡献。管理层也在季度报告里提到,对目前的市场和手上的订单保持乐观,有信心在今年继续稳定成长。从估值方面,目前PENTA的每股净利是12 cent。因此,以10倍PE推算,PENTA的潜在价值是每股RM1.20,依然还有20%上涨空间。值得一提的是,在未来当PENTA的BATU KAWAN新扩建设施完成后,它的产能将逐渐提升,业绩也预计会继续成长。

在2008全球陷入金融危机时,很多跨国公司撤出槟城,导致很多本地供应商受打击,一些甚至倒闭。PENTA也是受害者之一。当时,它在2008、2009、2010和2012年蒙受亏损,直到2014年业绩才开始稳定下来,持续赚钱。因此,PENTA在过去所打下的基础和积极改善业务,一步步走到现在确实不易。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 12-10-2016 08:44 PM

|

显示全部楼层

本帖最后由 哭哭鸟 于 12-10-2016 08:46 PM 编辑

https://www.evli.com/fund/pdf/fs_efm_en.pdf

| SYMBOL | COMPANY NAME | SHARE HOLDER | SHARE HELD | % OWNERSHIP | RANKING | ANNUAL REPORT | HOLDING DATE

| PENTA

| PENTAMASTER CORPORATION BERHAD | EVLI EMERGING FRONTIER

| 2,489,000 | 1.70% | 0 | Exclusive | 30/6/2016 | | PENTA | PENTAMASTER CORPORATION BERHAD | FONG SILING

| 2,000,000 | 1.40% | 10 | 2015 | 6/4/2016 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 3-11-2016 07:56 PM

|

显示全部楼层

本帖最后由 icy97 于 5-11-2016 04:48 AM 编辑

鹏达科技Q3净利涨34%

2016年11月5日

http://www.enanyang.my/news/20161105/鹏达科技q3净利涨34/

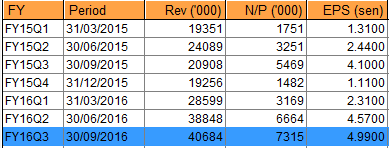

(吉隆坡4日讯)由于营业额亮眼,带动鹏达科技(PENTA,7160, 主板科技股)截至12月31日第三季,净利按年上涨33.75%。

该公司第三季净赚731万5000令吉,或每股净利4.99仙,超越上财年同季的546万9000令吉,或4.10仙。

而营业额则按年暴增94.59%,达到4068万4000令吉,主要归功于自动化设备和制造解决方案业务的收益增加,以及智能控制解决方案业务的盈利贡献。

累积9个月,公司净利按年剧增63.77%,至1714万8000令吉或每股净赚11.97仙;营业额则按年跃升68.04%,至1亿813万1000令吉。

展望前景,鹏达科技将持续专注于核心业务,并正面看待现财年的业务表现。

7160

| | Quarterly rpt on consolidated results for the financial period ended 30/09/2016 | | Quarter: | 3rd Quarter | | Financial Year End: | 31/12/2016 | | Report Status: | Unaudited | | Submitted By: |

|

|

| Current Year Quarter | Preceding Year Corresponding Quarter | Current Year to Date | Preceding Year Corresponding Period |

| 30/09/2016 | 30/09/2015 | 30/09/2016 | 30/09/2015 |

| RM '000 | RM '000 | RM '000 | RM '000 | | 1 | Revenue | 40,684 | 20,908 | 108,131 | 64,348 | | 2 | Profit/Loss Before Tax | 8,377 | 6,826 | 21,169 | 12,271 | | 3 | Profit/Loss After Tax and Minority Interest | 7,315 | 5,469 | 17,148 | 10,471 | | 4 | Net Profit/Loss For The Period | 8,138 | 6,060 | 18,785 | 10,642 | | 5 | Basic Earnings/Loss Per Shares (sen) | 4.99 | 4.10 | 11.97 | 7.86 | | 6 | Dividend Per Share (sen) | 0.00 | 0.00 | 0.00 | 0.00 |

|

|

| As At End of Current Quarter | As At Preceding Financial Year End | | 7 | Net Assets Per Share (RM) |

|

| 0.6708 | 0.5540 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 17-11-2016 01:39 PM

|

显示全部楼层

本帖最后由 icy97 于 17-11-2016 10:06 PM 编辑

冷眼推荐股(九):PENTA

Thursday, November 17, 2016

http://bblifediary.blogspot.my/2016/11/penta.html

业务

- 自动化设备器材(automated equipment)

- 自动化生产解决方案(automated manufacturing solutions)

PENTA(腾达科技,7160,主板科技股),成立于2002年2月26日,并于2003年7月23日上市大马交易所第二板,之后转至主板。

PENTA有两大核心业务,分别是设计和生产自动化设备器材(automated equipment)和自动化生产解决方案(automated manufacturing solutions),这些设备主要提供给半导体领域。

半导体领域目前占了PENTA总营业额的最大比重。

由于该领域的周期性明显, 而且竞争剧烈,因此为了缓冲半导体市场波动所带来的冲击, 该公司也积极探讨及开拓新产品, 如家居智能解决方案系统。

除了开发新产品,该公司也积极开发新市场,如汽车、药剂、医药、饮食、消费电子等。

在需求的增加,以及公司积极开法新产品和新市场下,终于看到了一些成果。

PENTA这家公司是我非常熟悉的公司,因为6月份时我在MYStockXplorer推荐过它,当时股价RM0.765。此外我也在这里介绍过它(参阅PENTA 乘胜追击),差不多4个月后开翻。

PENTA虽然在最新一季虽然仍然交出不错的业绩,营业额4068万令吉,净利也达到732万令吉,是近几年来的单季最高纪录。

然而,如果与上一季度做比较,营业额只是略微增长4.73%,而净利则增长了9.77%。

PENTA之前两个季度(FY16Q1 & FY16Q2)都是以爆炸式的倍增来成长的,相比之下这一季逊色了许多。

可以看出PENTA的营业额和净利增长已经开始放慢下来,而且我相信下个季度恐怕会滑落。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-11-2016 03:15 AM

|

显示全部楼层

美元走强.腾达股价获支撑

(吉隆坡17日讯)腾达机构(PENTA,7160,主板科技组)有望从美元汇率走强中受惠,因其80%营业额是以美元计算,仅有20%原料成本是以美元计。上述基本面及汇率利好,都可为该公司股价提供一些支撑。

丰隆研究指出,腾达机构主要涉足自动化器材制造,除了原本涉及半导体行业,目前已多元化至各行业领域,包括医药手套、饮食、发光二极体、物流、消费者电子、智慧型住宅及建筑方案等。

随着该公司股价最近从高峰回跌,加上美元汇率走高,股价出现反弹,全天扬升4仙或是3.05%至1令吉35仙。全天成交量为222万5100股,显示交投相当活络。

技术层面而言,预料1令吉29仙为其当前下跌支持水平,一旦跌破,短期内较为强稳的支持水平则落在1令吉24仙。至于当前上升阻力落在1令吉36仙,一旦突破则有望试探1令吉45仙。

文章来源:

星洲日报/财经‧2016.11.18 |

|

|

|

|

|

|

|

|

|

|

|

发表于 9-1-2017 07:34 PM

|

显示全部楼层

本帖最后由 icy97 于 12-1-2017 12:31 AM 编辑

腾达机构有信心1H17销售额将达到7,000万令吉以上

股市资讯研究团队 2017年 01月 09日 财经要闻

http://cj.sharesinv.com/20170109/42648/

腾达机构(Pentamaster Corporation)预期其1H17的销售额将会超越1H16。到目前为止,公司已录得总值约4,000万令吉的销售额,并且有信心能在1H17结束时达到7,000万令吉以上。

市场对测试器的需求应会保持殷切,由于市面上的智能电讯产品与日俱增。公司目前约一半的订单是来自智能器材领域,其余订单则是来自汽车业。预期半导体测试器的贡献将占公司收入的约60%。

公司计划在今年专心扩充其智能自动化生产机械业务。该业务得以取得增长是由于马来西亚的企业希望能在高精密工程与制造方面以机械来取代人工。

启示:腾达机构位于峇都加湾(Batu Kawan)总值2,500万令吉的新厂房将于2017年下半年动工,并计划于2018年中开始生产智能自动化生产机械。预期该业务将于2017年带来的贡献将占公司收入的约15%,之前的份额约为5%。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 11-1-2017 10:33 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 27-1-2017 06:14 AM

|

显示全部楼层

Type | Announcement | Subject | OTHERS | Description | Error made in Notice of Interest of Substantial Shareholder pursuant to Section 69E and 69B of the Companies Act, 1965 (Form 29A & Form 29B) | Pentamaster Corporation Berhad (“PMCB” or “the Company”) wishes to announce that it has on 26January 2017 received a letter from Pheim Asset Management Sdn Bhd (“PHEIM”) informing the Company that the substantial shareholder notifications (Form 29A and Forms 29B) that PHEIM had sent to the Company had been done in error. The Form 29A and Forms 29B were received from PHEIM and duly announced by the Company during the period from 22 September 2016 to 23 January 2017.

PHEIM informed that it has been advised that PHEIM had at no time been a substantial shareholder of PMCB nor had any of the funds under its management. Shares purchased by PHEIM had been for the account of its various managed funds which individual holding had been all below the 5% reporting threshold during those reporting periods.

This announcement is dated 26 January 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 7-2-2017 06:53 PM

|

显示全部楼层

本帖最后由 icy97 于 8-2-2017 03:50 AM 编辑

伟特与腾达购槟城地 发展自动化集群

By Sulhi Azman / theedgemarkets.com | February 7, 2017 : 8:34 PM MYT

http://www.theedgemarkets.com/my/article/伟特与腾达购槟城地-发展自动化集群

(吉隆坡7日讯)由伟特机构(Vitrox Holdings Bhd)和腾达(Pentamaster Corp Bhd)拥有的公司,以352万令吉收购位于槟城峇都加湾工业园的一幅5.05英亩地。

伟特机构和腾达今日向大马交易所报备,Penang Automation Cluster私人有限公司向槟州发展机构(Penang Development Corporation)购买该地。

这两家公司指出,这幅地将用于发展和经营一个中小型自动化工业集群,并称这将支持其长期策略,提供更广泛的高端自动化检测设备,以发展业务。

一旦获得环境部批准,伟特机构和腾达预计,该集群将进行包括精密工程和钣金加工、模具、机械加工、精加工和涂层服务的活动。

“自动化集群预计将于2017年下半年开始建设,发展期为两年。”

伟特机构和腾达的初步估计显示,可能需要拨出2300万令吉投资在自动化集群。

这两家公司补充:“自动化集群仍处于初步规划阶段。”

伟特机构和腾达各持有Penang Automation Cluster的35%股权,而第三名股东是Walta Engineering私人有限公司,持30%。

(编译:陈慧珊)

Type | Announcement | Subject | OTHERS | Description | Acquisition of a Property by a Joint Venture Company namely, Penang Automation Cluster Sdn Bhd (Company No 1192380-V) ("PAC") wherein Pentamaster Technology (M) Sdn Bhd (Company No 336488-H) ("PTSB"), a wholly owned subsidiary company of PMCB holds 35% equity interest in the issued and paid up capital of PAC | 1. INTRODUCTION The Board of Directors of PMCB wishes to announce that PAC (the “Purchaser”), a 35%-owned investee of PTSB, has on 7 February 2017 entered into a Sale and Purchase Agreement (the “SPA”) with THE PENANG DEVELOPMENT CORPORATION (the “Vendor”) for the acquisition of a piece of land as detailed in Section 4.1 of the SPA (the “Property”) at a total consideration of Ringgit Malaysia Three Million Five Hundred and Twenty Thousand Seven Hundred and Sixty Three and Sen Twenty (RM3,520,763.20) only (the “Purchase Price”) [the “Acquisition”].

2. BACKGROUND INFORMATION 2.1 Information on PAC PAC was incorporated in Malaysia as a private limited company under the Companies Act, 1965 on June 24, 2016. PTSB has on January 16, 2017 entered into a Joint Venture Shareholders’ Agreement (the “Agreement”) with Vitrox Corporation Berhad (Company No 649966-K) ("VCB") and Walta Engineering Sdn Bhd (Company No 270199-T) (“WESB”) to establish a Joint Venture Company through PAC wherein PTSB, VCB and WESB will subscribe 35%, 35% and 30% of the issued and paid up capital of PAC respectively (the “JV”). PAC’s principal activities are providing Technological Design, Research, Value Added Engineering Development, Metrology Shared Services, 3-D prototyping, Smart Manufacturing System and Technical Training to the Automation Cluster Companies specialized in the area of Design, Development and manufacture of high precision metal fabrication components, modules and systems for semiconductor, electronics, automotive, aerospace and other high growth industries in the region. As at the date of the announcement, PAC has a share capital of RM3,000,000.00. The existing directors and shareholders of PAC are as follows:- Directors 1. Chu Jenn Weng 2. Chuah Choon Bin; and 3. Goh Kheng Sneah. Shareholders and shareholdings a. PTSB (35%); b. VCB (35%); and c. WESB (30%)

2.2 Information on VCB VCB was incorporated in Malaysia on 22 April 2004 under the Companies Act, 1965 as a private limited company under the name of ViTrox Corporation Sdn Bhd. On 24 June 2004, it was converted into a public limited company and adopted its present name. VCB is a company listed on the Main Market of Bursa Malaysia Securities Berhad. As at the date of the announcement, VCB has a share capital of RM23,475,795. VCB is principally involved in investment holding and development of 3D and line scan vision inspection system. The Directors of VCB are Dato’ Seri Dr. Kiew Kwong Sen, Chu Jenn Weng, Siaw Kok Tong, Yeoh Shih Hoong, Chuah Poay Ngee, Prof. Ir. Dr. Ahmad Fadzil Bin Mohamad Hani and Chang Mun Kee.

2.3 Information on the WESB WESB was incorporated in Malaysia on July 16, 1993 under the Companies Act, 1965 as a private limited company under its present name. As at the date of the announcement, WESB has a share capital of RM4,900,000. WESB is principally engaged in the manufacturing of machinery, equipment and tester and fabrication of machinery parts, tools and dies. The Directors and Shareholders of WESB are Goh Kheng Sneah and Liong Swee Yen.

2.4 Information on the Vendor THE PENANG DEVELOPMENT CORPORATION, is a body corporate incorporated under the Penang Development Corporation Enactment, 1971 and having its office at Bangunan Tun Dr Lim Chong Eu, No 1 Pesiaran Mahsuri, Bandar Bayan Baru, 11909 Bayan Lepas, Penang. The Vendor was establised with the following objectives:- - To spearhead Penang’s socio-economic development

- To assist in eradicating poverty and creating employment opportunities

- To improve the quality of life for the people of Penang

The core activities of the Vendor, a self-funding statutory, are:- - Land Development

- Investment

- Entrepreneur Development

3. INFORMATION ON THE JV 3.1 Rationale for the JV The purposes of JV are:- 1. To build the local supply chain ecosystem 2. To fund the development 3. To manage the supply chain ecosystem In view of the above and pursuant to the Agreement, PAC is to acquire the Property solely for the purpose of developing and managing a small medium industry cluster which include the activity of precision engineering and sheet metal fabrication, tooling, machining, finishing and coating services to be carried out by the Purchaser and/or its tenants (as the case may be) [“Automation Cluster”] and as approved by the Department of Environment, Ministry of Natural Resources and Environment Malaysia. The JV will enable PMCB to build a robust and reliable supply chain ecosystem in the country that supports PMCB’s long-term strategy to grow its business in providing a wider range of high-end automated equipment supporting various industries globally. The Automation Cluster is expected to commence construction in 2nd half of 2017 and span over a development period of within two years. As at the date of the announcement, no development approvals have been obtained for the Automation Cluster and PAC estimated an investment value of RM23 million for the Automation Cluster. The Automation Cluster is still in its initial planning stage and therefore, the above information is preliminary at this juncture and may be subject to further refinement.

3.2. Salient Terms of the Agreement 3.2.1 Equity structure Unless agreed by PTSB, VCB and WESB (“JV Parties”) in writing, the total issued and paid up share capital of PAC shall as the Completion Date and at all times herein be held by the JV Parties in the following proportions: Shareholder | Percentage | PTSB | 35% | VCB | 35% | WESB | 30% | Total | 100% |

3.2.2 Termination and winding-up Except for the provisions in the Agreement which shall continue in full force after termination, the Agreement shall terminate: (a) when, as a result of transfers of shares made in accordance with the Agreement or the Articles of Association of PAC, only one JV Party remains as legal and beneficial holder of the shares in PAC; or (b) when a resolution is passed by shareholders or creditors, or an order made by a court or other competent body or person instituting a process that shall lead to PAC being wound up and its assets being distributed among the PAC's creditors, shareholders or other contributors; or (c) the termination of the SPA for whatsoever reason.

4. DETAILS OF THE ACQUISITION 4.1 Information on the Property The Property is known as all that piece of land situated in Daerah Seberang Perai Selatan and forming part of Mukim 13, Seberang Perai Selatan the site whereof is marked Plot SV61 Batu Kawan Industrial Park and delineated and edged in red and marked “A” on the plan annexed in the SPA and containing an area of 5.0516 acres. The said Property is at present vested in the State Authority of Penang (“the State Authority”). The Property is to be alienated by the State Authority to the Vendor in accordance with the National Land Code, 1965 (‘the NLC’) for a term of thirty (30) years under Qualified Title and ultimately to be held under a State Lease subject to the category of land use, the express conditions and the restrictions in interest as shall be imposed by the relevant authorities and the Property and any building erected thereon shall be used only for ‘developing and managing the Automation Cluster and to carry out all its obligations under the SPA which include the activity of precision engineering and sheet metal fabrication, tooling, machining, finishing and coating services to be carried out by the Purchaser and/or its tenants (as the case may be) and as approved by the Department of Environment, Ministry of Natural Resources and Environment Malaysia.’ (the “Land Use”). Pursuant to the SPA, the Property is to be acquired upon such alienation free from all encumbrances on an ‘as is where is basis’ save and except for the earthworks as described in Clause 10.2 of the SPA as backfilling of the Property up to 2.23 metres (“the Earthworks”) and provisions of infrastructure i.e. provision of roads, drainage and sewerage servicing the Property and water, electricity and telecommunication mains for connection to the Property for the benefit of the Property (“the Infrastructure”), and with legal possession but subject to the category of land use, the express conditions and the restrictions in interest as shall be imposed by the relevant authorities, all conditions and restrictions implied by the NLC and upon the terms and conditions of the SPA. PAC is unable to provide the information on Net Book Value of the Property as PAC is not privy to this information.

5. APPROVALS REQUIRED The JV was not subject to approval from the shareholders of PMCB and/or any regulatory authority(ies). The JV also was not conditional upon any other corporate proposals undertaken or to be undertaken by PMCB. Save for the State Authority for the alienation of the Property to the Vendor, the Acquisition is not subject to approval being obtained from the shareholders of PMCB and/or any regulatory authority(ies).

6. MAJOR SHAREHOLDERS’ AND DIRECTORS’ INTERESTS To the best of the knowledge of the Board of Directors of PMCB, none of the Directors and/or major shareholders of PMCB, or persons connected to them, has any interest, direct or indirect:- a) in the JV; and b) in the Acquisition.

7. DIRECTORS’ STATEMENT The Board of Directors of PMCB is of the opinion that the JV is in the best interest of the PMCB Group.

8. ESTIMATED TIMEFRAME FOR COMPLETION The JV is expected to be completed within 12 months period from the date of Agreement. The Acquisition is expected to be completed within 12 months period from the date of SPA.

This announcement is dated 7 February 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-2-2017 12:28 PM

|

显示全部楼层

1.67是52周新高..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 11-2-2017 07:00 AM

|

显示全部楼层

Type | Reply to Query | Reply to Bursa Malaysia's Query Letter - Reference ID | IQL-08022017-00002 | Subject | ACQUISITION OF A PROPERTY BY A JOINT VENTURE COMPANY NAMELY, PENANG AUTOMATION CLUSTER SDN BHD (COMPANY NO 1192380-V) (PAC) WHEREIN THE COMPANY HOLDS 35% EQUITY INTEREST IN THE ISSUED SHARE CAPITAL OF PAC [THE ACQUISITION] | Description | Pentamaster Corporation Berhad (PMCB or Company) - Acquisition of a Property by a Joint Venture Company namely, Penang Automation Cluster Sdn Bhd (Company No 1192380-V) (PAC) wherein Pentamaster Technology (M) Sdn Bhd (Company No 336488-H) (PTSB), a wholly owned subsidiary company of PMCB holds 35% equity interest in the issued and paid up capital of PAC (the Acquisition) | Query Letter Contents | We refer to your Company’s announcement dated 7 February 2017, in respect of the aforesaid matter. In this connection, kindly furnish Bursa Securities with the following additional information for public release:- 1. The eventual issued share capital of PAC. 2. The breakdown of the total capital and investment outlay in the PAC by Pentamaster Corporation Berhad thereof. 3. The sources of funding by PAC for the purchase consideration of the Property, and the cost of development/construction of the Automated Cluster, and the breakdown. 4. A statement by the board of directors, excluding interested directors stating whether the Acquisition is in the best interests of the Pentamaster Corporation Berhad Group. | Unless stated otherwise, definitions used in this announcement shall carry the same meaning as defined in the announcement dated February 7, 2017 in relation to the Acquisition.

With reference to Bursa Malaysia Berhad’s query letter dated February 8, 2017 (Reference Number : IQL-08022017-00002), the Board of Directors of PMCB wishes to inform/clarify the following:- 1. The eventual issued share capital of PAC. The eventual issued share capital of PAC is RM3,000,000.00.

2. The breakdown of the total capital and investment outlay in the PAC by Pentamaster Corporation Berhad thereof. PMCB holds 35% of the issued share capital of PAC and hence, the total capital and investment outlay is RM1,050,000.00.

3. The sources of funding by PAC for the purchase consideration of the Property, and the cost of development/construction of the Automated Cluster, and the breakdown. The Purchase Price of the Property and the cost of development/construction of the Automation Cluster will be financed via PAC’s capital and bank borrowings. The breakdown of which are as follows:- Description | RM (Million) | Purchase Price of the Property | 3.5 | Cost of development/construction of the Automation Cluster | 19.5 | Total | 23.0 |

Funded by: | RM (Million) | Capital of PAC | 3.0 | Bank borrowings | 20.0 | Total | 23.0 |

No development approvals have been obtained for the Automation Cluster yet and the Automation Cluster is still in its initial planning stage. Therefore, the cost of development/construction of the Automation Cluster and the amount of funding required is a preliminary estimate at this juncture and may be subject to further refinement.

4. A statement by the board of directors, excluding interested directors stating whether the Acquisition is in the best interests of the Pentamaster Corporation Berhad Group. The Board of Directors of PMCB is of the opinion that the Acquisition is in the best interest of the PMCB Group.

This announcement is dated February 10, 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-2-2017 07:32 PM

|

显示全部楼层

本帖最后由 icy97 于 28-2-2017 01:53 AM 编辑

7160

| | Quarterly rpt on consolidated results for the financial period ended 31/12/2016 | | Quarter: | 4th Quarter | | Financial Year End: | 31/12/2016 | | Report Status: | Unaudited | | Submitted By: |

|

|

| Current Year Quarter | Preceding Year Corresponding Quarter | Current Year to Date | Preceding Year Corresponding Period |

| 31/12/2016 | 31/12/2015 | 31/12/2016 | 31/12/2015 |

| RM '000 | RM '000 | RM '000 | RM '000 | | 1 | Revenue | 43,476 | 19,256 | 151,607 | 83,604 | | 2 | Profit/Loss Before Tax | 7,337 | 2,411 | 28,506 | 14,682 | | 3 | Profit/Loss After Tax and Minority Interest | 9,548 | 1,482 | 26,696 | 11,953 | | 4 | Net Profit/Loss For The Period | 10,468 | 1,648 | 29,253 | 12,290 | | 5 | Basic Earnings/Loss Per Shares (sen) | 6.51 | 1.11 | 18.53 | 8.97 | | 6 | Dividend Per Share (sen) | 0.00 | 0.00 | 0.00 | 0.00 |

|

|

| As At End of Current Quarter | As At Preceding Financial Year End | | 7 | Net Assets Per Share (RM) |

|

| 0.7332 | 0.5540 |

|

| | |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 5-3-2017 10:22 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 8-3-2017 04:26 PM

|

显示全部楼层

差不多要破2.00了..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 1-4-2017 01:54 AM

|

显示全部楼层

本帖最后由 icy97 于 1-4-2017 04:32 AM 编辑

Does Pentamaster’s rally still have legs?

Wei Lynn Tang | 31 Mar 2017 00:30

http://www.focusmalaysia.my/Mainstream/does-pentamaster-s-rally-still-have-legs

The rally in Penta-master Corp Bhd’s shares doesn’t seem to be stopping – already, the counter has surged fourfold in the past 12 months.

Year to date, it has risen 78%. This is a feat considering it beat the FBM KLCI’s 7% gain by 11 times and is double the 39% increase chalked up by Bursa Malaysia’s Technology Index in the same period.

Equally, earnings of the Penang-based automated equipment company have grown from strength to strength – leapfrogging from RM3 mil in the first quarter ended March (Q1 2016), to RM9.5 mil in the final quarter of FY16.

On an annual basis, its FY16 earnings per share doubled to 18.5 sen.

‘Not overvalued yet’

Some may attribute the persistent rise in Pentamaster’s shares partially to its low base. Nonetheless, at a price of RM2.40 on March 28 – its highest in more than 10 years – its price-to-earnings multiple (PER) comes to 12 times.

“If you look at the technology sector, the average PER is around 14 to 18 times. Ours is less than 12 times. If we continue to grow, our share price (now) is still reasonable, it is not overvalued yet,” group executive chairman Chuah Choon Bin tells FocusM.

Chuah, who holds 21.5% in the company, however, appears to be indifferent to the rally in its shares, saying he has not been marketing his stock to analysts.

No research house covers Penta--master.

In fact, Chuah credits it all to the group’s research and development (R&D) efforts four years back – venturing into high-end technology for smart devices – which has now started to bear fruit.

Chuah also affirms he is not retiring in the immediate future. This comes amid market talk that he could be stepping down.

“I am 56 this year, but no, I am not leaving anytime soon,” he says.

Chuah, an engineer by profession, co-founded Pentamaster, and has been instrumental in leading the group since 1991.

While acknowledging that the semiconductor industry is a cyclical one, Chuah is still positive on its prospects this year – and expects the sector to account for 80% of group revenue.

“We have orders in hand to keep us busy until the second half of the year. Performance-wise, we are (still) forecasting a double-digit growth in revenue and profit,” he says.

Having come off a strong FY16, however, this year’s growth rate will not be as good as last year’s, he adds.

“We managed to leapfrog in 2016 because we penetrated a new customer base – these are premium customers into higher-end products and more stringent requirements. They can give us longer-term forecast, better visibility and continuation in orders,” Chuah explains.

He adds that being good paymasters, this customer base helped, too.

The World Semiconductor Trade Statistics has raised its 2017 global semiconductor sales forecast growth from 3.3% to 6.5% to reach US$361 bil (RM1.6 tril), and up by 2.3% to hit US$369 bil next year.

To maintain margins

In the meantime, Chuah says the group should be able to maintain its margins at last year’s level, as its bottom line grows proportionately with the top line.

Pentamaster’s FY16 net margin came in at almost 18%, higher than 2015’s 14%. Gross margins meanwhile were at 32% versus 29%.

This comes as its net profit more than doubled to RM26.7 mil from RM12 mil. Revenue grew 81% to RM151.6 mil from RM83.6 mil.

In Q4FY16 alone, Pentamaster’s net profit surged over 500% year-on-year to RM9.5 mil, while revenue rose 125% to RM43.5 mil.

While there was a tax credit of RM3.1 mil, a large part of the growth was driven by higher demand for test equipment from the semiconductor market, especially the smart device sector – such as camera, microphone, position sensor MEMS and light sensor.

“We achieved higher revenue (also) because our average selling price increased,” Chuah shares, adding that a machine costing less than US$200,000 previously now sells for more than US$500,000.

The automated equipment segment is the group’s biggest revenue contributor, and also delivers the highest margin of 27%, compared to the 8-12% achieved by its automated manufacturing solution and smart control solution system segments.

“Pentamaster builds 5-in-1 test handlers, or essentially, a testing machine. 5-in-1 means there are five test parameters in one machine. This type of machines are more complex than most other machines,” an industry observer quips.

Basically, the group manufactures automated equipment and precision machinery components for the medical and consumer electronics sectors.

These engineering or manufacturing equipment have to be tested before being released to the public for safety regulations and quality controls.

Going forward, Chuah expects demand for testers to remain positive, as the number of new smart telecommunication and automotive products in the market increase.

“Today, many of the end-products have better functions and features – 3D, camera resolution, wireless, etc. The requirement for smart technology is higher now, there’s no longer any use for manual tracking,” he says.

Chuah expects growth for Pentamaster’s newly-ventured-into smart control solution system to pick up pace only next year, when the construction and property market recovers.

“The strong US dollar also benefits us, as we export 80% of our sales which are traded in USD.

However, we also buy in USD, so the exchange rate really just makes us more competitive, as we continue to move our product range higher across the value chain,” he says.

As much as the automation industry is booming, Chuah however highlights his concern that our education system does not train enough engineers in this field, and thus, not churning out talents.

Strong cash flow

Pheim Asset Management first emerged as a substantial shareholder in Pentamaster on Sept 22 last year with a 5.1% stake. It has since increased its stake to 6.3% as of Jan 20.

Asked on Pheim’s interest, Chuah says: “It still sees opportunity for Pentamaster to grow. According to Pheim, our PER is still very low.”

An analyst, while agreeing that PER should be considered when picking a stock, also points out the importance of a company’s cash flow.

For the 12 months ended Dec 31 last year, Pentamaster generated RM20 mil in cash from operations compared with RM8.6 mil the year before.

This could place the group in a still comfortable position, when it uses its RM30 mil net cash balance to expand capacity, as Chuah has stated he “would not want to take on debt if possible”.

“We are spending RM25 mil on capex to construct our new facility (which will double our capacity) in Batu Kawan, which includes the remaining 40% of the land cost. But we will spend it in phases. This year, we are looking at spending RM10 mil as construction begins," Chuah says.

The new facility has a manufacturing space of 90,000 sq ft on a 1.28ha industrial plot, and will house the group’s automated solutions segment.

It is worth noting that different technology companies operate in different segments of the industry and ecosystem.

Among the few technology players, Phillip Capital Management chief investment officer Ang Kok Heng likes ViTrox, given its better growth prospects.

While stocks in the technology sector have rallied in the past six months to a year, it is ultimately earnings delivery that will continue to drive investor interest and share price momentum.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 17-4-2017 03:29 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 18-4-2017 03:24 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 18-4-2017 03:26 PM

|

显示全部楼层

已經破 > 3.00了..

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3489

3489  112

112