|

|

发表于 27-4-2017 07:07 PM

|

显示全部楼层

发表于 27-4-2017 07:07 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 4-5-2017 03:51 PM

|

显示全部楼层

3.17了..

|

|

|

|

|

|

|

|

|

|

|

|

发表于 9-5-2017 06:01 PM

|

显示全部楼层

本帖最后由 icy97 于 10-5-2017 02:06 AM 编辑

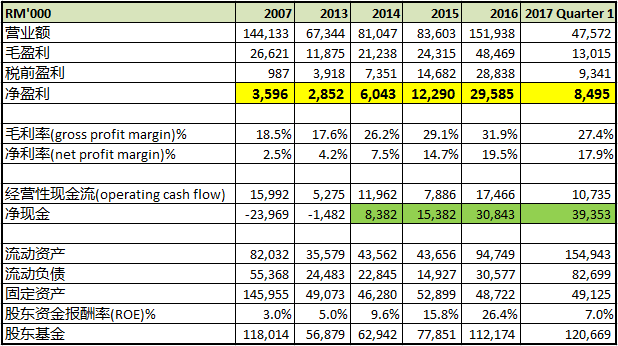

SUMMARY OF KEY FINANCIAL INFORMATION

31 Mar 2017 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Mar 2017 | 31 Mar 2016 | 31 Mar 2017 | 31 Mar 2016 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 47,572 | 28,599 | 47,572 | 28,599 | | 2 | Profit/(loss) before tax | 9,341 | 4,238 | 9,341 | 4,238 | | 3 | Profit/(loss) for the period | 8,495 | 3,402 | 8,495 | 3,402 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 7,538 | 3,169 | 7,538 | 3,169 | | 5 | Basic earnings/(loss) per share (Subunit) | 5.14 | 2.31 | 5.14 | 2.31 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.7896 | 0.7382

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-5-2017 02:07 PM

|

显示全部楼层

本帖最后由 icy97 于 10-5-2017 11:47 PM 编辑

PENTA, 鹏达科技下个季度业绩是否还会创新高?

Author: Spencer88 | Publish date: Wed, 10 May 2017, 09:56 AM

https://klse.i3investor.com/blogs/spencer88/122525.jsp

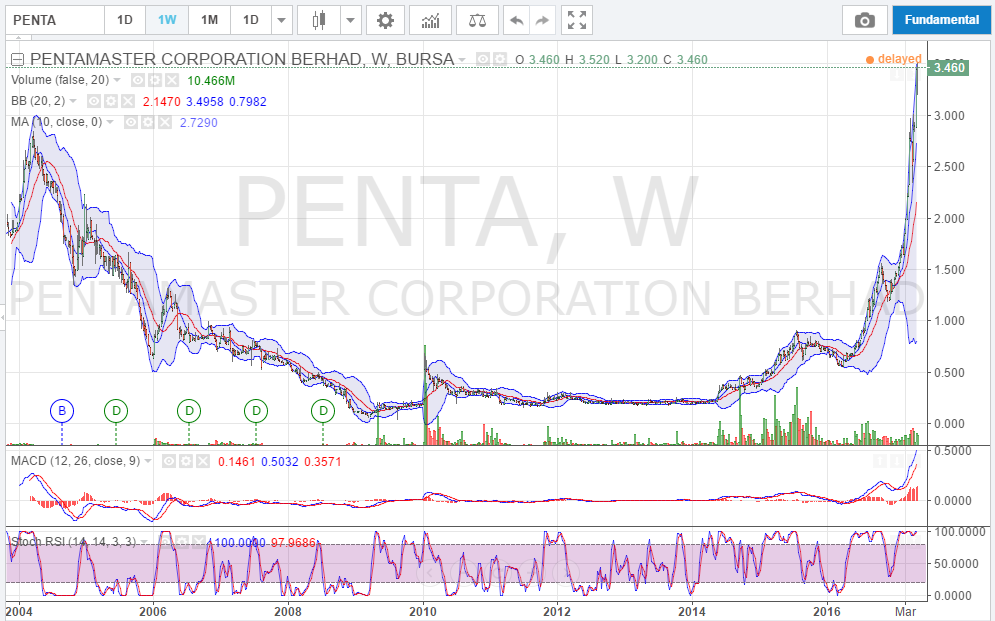

相信有跟进 PENTA 的股友应该不难发现 PENTA 的第一季度业绩已经在昨天出炉,业绩可说是标青,这个季度的七百五十万令吉税后盈利比起去年第一季度的三百一十万令吉高出了整整138%!这也解释了为什么 PENTA 的股价在近期内大幅度偷步上升的原因,然而笔者今天在这里要讨论的亦不是PENTA 的盈利,因为只要有阅读季度报告的股友都不难发现盈利增长的原因。今天主要要讨论的是PENTA 的展望(Prospect) 以及笔者在 PENTA 的 Balance Sheet 里所发现的小小细节,希望这个小小细节有助于各位股友们做出该继续持有还是卖出的决定。

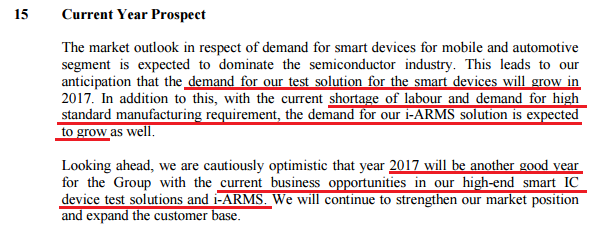

在这里我们先谈管理层对 PENTA 的展望,在这里不多解释相信只要会阅读的股友们应该不难明白,整体来说管理层主要提及的是市场对 PENTA 产品的需求量将会增加,至于增加多少就不得而知了。

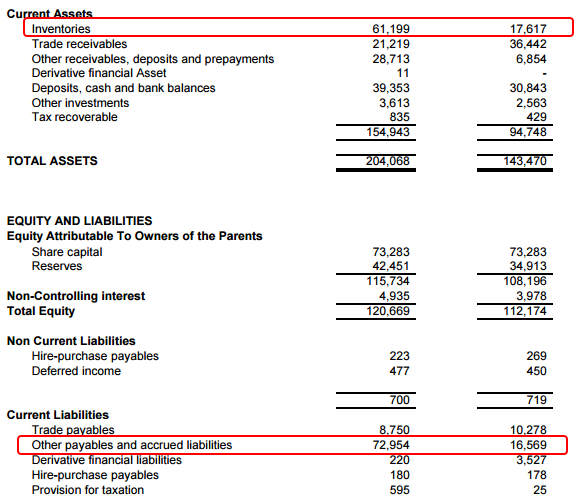

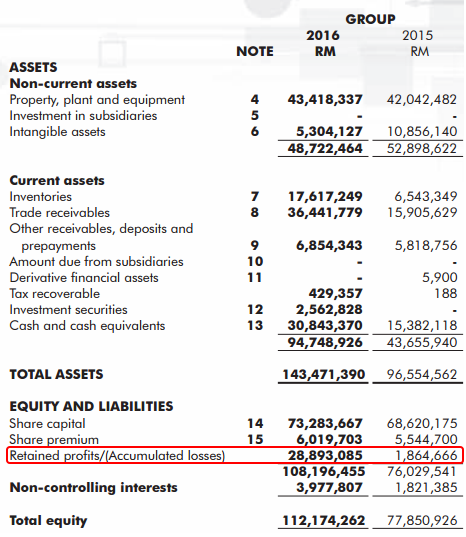

但是接下来笔者将为大家分享有一点应该值得大家去研究以及分析的部分,因为笔者认为这个部分极有看头。从生意角度来看,除了应收账款(Trade Receivables) 以外,存货(Inventory) 应该将会是一门生意的现金流(Cash Flow) 被锁定的地方。而一门生意要是没有一定的需求的话,逻辑上来说我们应该不会盲目的把生意的现金流锁死在存货里,要是存货卖不出的话,生意将会面临周转不灵的问题出现。如果大家有注意的话,PENTA 的存货在这个季度比起历年来的季度存货出奇的高,而存货相信不是以现金来支付,因为其他应付账款(Other Payables) 也比上个季度高出了整整五千七百万令吉,所以笔者推测 PENTA 的存货应该是以欠款的方式先购买,随后再偿还。为了省下大家的时间笔者在这里为大家准备了PENTA 从2015财年第一季度至最新季度的存货图表以供大家参考及讨论。

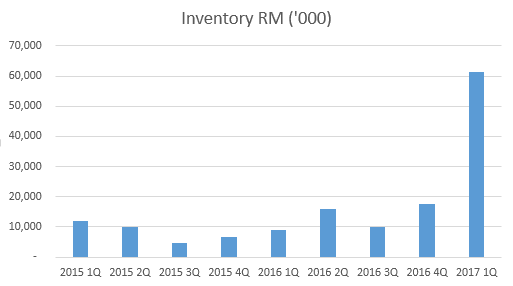

大家可以看见PENTA的存货在过去八个季度以来从来不曾超过两千万令吉的水平,然而在这个季度却大幅度的飙升至六千万以上的水平!笔者以生意人的角度来思考,要是我们的产品没有一定的需求的话,身为老板的我们应该不会盲目的囤货吧?而且囤货水平不是比平常高了一些,而是比起过往八个季度的平均存货水平高了整整4-5倍!!而PENTA 接下来的季度是否还有看头,那就要考考大家的眼光了。由于以上的简单分析都是笔者的推测以及个人看法,因此不能做准也请大家不要盲目的买进或卖出,买卖自负!希望这个简单的分析能够帮助到大家,要是大家有任何看法的话,可以留言大家一起探讨也许会有不同的结果。

|

评分

-

查看全部评分

|

|

|

|

|

|

|

|

|

|

|

发表于 13-5-2017 02:43 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 14-5-2017 12:22 PM

|

显示全部楼层

本帖最后由 icy97 于 15-5-2017 12:09 AM 编辑

昨天发表的PENTA基本面分析中有点小出错,笔者老眼昏花错看trade payable 暴涨,实际上是 other payable 暴涨,而这两个词汇代表不同的意思,因此笔者决定修改文章部分内容。谢谢大家的留言和意见回馈让我们做到更好,感恩!

修改后的内容:

此外,Other payable 也暴涨至RM73million,根据2016年年报对Other payable的诠释,这包括deposit from customers upon placing sales orders。这点更为印证笔者的推测 – 大量的订单让PENTA生产或购买大量的存货。

WeShare & WeTrade

|

|

|

|

|

|

|

|

|

|

|

|

发表于 20-5-2017 03:05 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 10-6-2017 03:14 AM

|

显示全部楼层

本帖最后由 icy97 于 18-6-2017 07:25 AM 编辑

鹏达600万增持子公司40%

http://www.sinchew.com.my/node/1651453/

(吉隆坡10日讯)鹏达机构(PENTA,7160,主板科技组)以600万令吉增持Penta Instrumentation私人有限公司剩余12万股或40%股权,成为独资子公司。

根据文告,该公司在收购其余股权之前,持有Penta Instrumentation公司的18万股或60%股权,在增持至100%的股权后,将全数拥有其30万股。

创于2003年的Penta Instrumentation公司,主要为电器和电子领域提供自动化测试设备、测试及测量系统的设计和制造。

文章来源:

星洲日报/财经·2017.06.10

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

NON RELATED PARTY TRANSACTIONS | Description | Acquisition of remaining 40% shareholding in Pentamaster Instrumentation Sdn. Bhd. | The Board of Directors of Pentamaster Corporation Berhad ("PMCB" or "the Company") wishes to announce that the Company acquired the remaining 40% shareholding in its subsidiary company Pentamaster Instrumentation Sdn Bhd (Company No. 637373-M) (“PISB”) comprising 120,000 ordinary shares (“the Shares”) each fully paid up for a total cash consideration of Ringgit Malaysia Six Million (RM6,000,000.00) only on 9 June 2017.

Please refer to the attached file for details. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5457929

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-6-2017 11:50 PM

|

显示全部楼层

本帖最后由 icy97 于 11-6-2017 01:19 AM 编辑

热股讨论:半导体行业持续发热,PENTA全购子公司股份

2017年6月10日星期六

http://wesharenwetrade.blogspot.my/2017/06/penta_10.html

过去一周,半导体相关行业的股持续发热。先有JHM宣布派发bonusshare,然后4月份全球半导体领域成长高达21%,然后FRONTKEN以RM13.3million增持台湾子公司11.42%股权,至84.6%。而昨天PENTA亦宣布全购子公司剩余的股份。

先说说FRONTKEN的收购新闻,在这之前笔者对FRONTKEN根本不了解。这项收购出炉后,其股价从29仙涨至32仙,短短3天都有10%涨幅,相当不赖。虽然只增持11.42%股份,可是对FRONTKEN集团的净利影响不小,即使净利没有成长,亦因为这家子公司相当赚钱,纳入此11.42%股份已足以让FRONTKEN净利至少成长10%以上。

至于PENTA也不逞多让,以RM6million收购子公司PISB剩余40%的股份,成为独资子公司。PISB主要生产automatedtesting equipment and test and measurement systems,是PENTA目前最赚钱的业务。2016年PISB的净利达到RM6.4million,40%的股份就表示RM2.56million的净利,这让PENTA的净利即使在没有成长的情况下因此股份增加而净利上升10%左右。

2017年第一季度PISB 40%的股份就贡献RM957,000净利(去年同期才RM233,000)。所以PENTA以RM6million收购40%的股份,换来至少RM2million以上的净利贡献,实在是好便宜。如果是收购全新的子公司可能还要经历管理层,运作磨合等风险,但是这项收购几乎是没有风险的,因为PISB已经是PENTA超过10年60%股份的子公司了。

自今年与Vitrox联合收购土地后,此收购是PENTA今年第二项大投资活动。PENTA目前的净现金达RM39million,足以现金支付RM6million的收购价。由于PENTA没派发股息的打算,存有高额现金的PENTA未来或许还有大动作。

至于PENTA的收购消息能否像FRONTKEN在下周开市后股价迎来上升?很难说,因为没人能准确预测股价的走势,而且之前PENTA的股价已偷步上涨至RM3.79。无论如何,笔者对这项收购对PENTA长期发展和利益相当乐观。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 19-6-2017 04:43 AM

|

显示全部楼层

发表于 19-6-2017 04:43 AM

|

显示全部楼层

本帖最后由 icy97 于 20-6-2017 06:19 AM 编辑

拓自动化解决方案商机

腾达拟分拆业务赴港上市

2017年6月14日

(吉隆坡13日讯)腾达科技(PENTA,7160,主板科技股)考虑将旗下自动化解决方案业务,带到香港交易所主板独立上市。

腾达科技向交易所报备,上市建议的细节还有待落实,不过,在完成此交易之前,公司会把涉及自动化解决方案业务的子公司进行重组。

而成功上市后,这些子公司将持续保留在腾达科技旗下。

为了在香港挂牌,该公司已经向开曼群岛的公司注册处提出申请,在当地成立一家子公司,名为Pentamaster国际有限公司,主要业务是投资控股。

腾达科技解释,建议独立上市的原因包括,这可让自动化解决方案业务得到认可,进一步巩固企业的名誉,因这可拓展客户规模。

另外,也能更清晰地隔离业务责任和营运,进而提升效率。这样一来,相关的管理团队就能专注于自动化解决方案业务的商机。

挂牌时间未定

不仅如此,这预计能释放股东的价值,且能通过香港股票市场多元化的平台融资,为未来增长资金提供融资灵活度。

腾达科技不忘强调,独立上市建议目前处于最初阶段,需要相当广泛的准备工作,因此仍无法敲定上市时间。【e南洋】

Type | Announcement | Subject | OTHERS | Description | PENTAMASTER CORPORATION BERHAD ("PCB" OR THE "COMPANY")- PROPOSED LISTING OF THE COMPANY'S AUTOMATED SOLUTION BUSINESS ON THE MAIN BOARD OF THE STOCK EXCHANGE OF HONG KONG LIMITED ("PROPOSED LISTING"); AND- PROPOSED INCORPORATION OF A WHOLLY-OWNED SUBSIDIARY COMPANY. | 1. INTRODUCTION The Board of Directors of PCB (“Board”) wishes to announce that the Company is considering the pursuit of a separate listing of its automated solution business on the Main Board of the Stock Exchange of Hong Kong Limited (“HK Stock Exchange”).

Details of the Proposed Listing have yet to be determined. However, prior to the completion of the Proposed Listing, PCB will undertake a reorganisation of its subsidiaries involved in the automated solution business and these subsidiaries will continue to remain as subsidiaries of PCB upon completion of the Proposed Listing. A detailed announcement in relation to the Proposed Listing will be made in due course, once the Company has finalised and approved the structure of the Proposed Listing.

To facilitate the Proposed Listing, an application has been made to the Registrar of Companies in the Cayman Islands to incorporate a wholly-owned subsidiary company, namely Pentamaster International Limited ("PIL") in the Cayman Islands on 12 June 2017. The principal activity of PIL is that of investment holding. The Company will make further announcement in due course upon the receipt of the Certificate of Incorporation from the Registrar of Companies in the Cayman Islands. None of the Directors and/or major shareholders of PCB or persons connected to them have any interest, direct or indirect, in the proposed incorporation of PIL.

2. RATIONALE AND BENEFITS OF THE PROPOSED LISTING The rationale and benefits of the Proposed Listing are as follows: (i) The Proposed Listing will enable the automated solution business to gain recognition and corporate stature through the listing status of its own and further enhance its corporate reputation which will assist in expansion of its customer base; (ii) The Proposed Listing will enhance efficiency by way of promoting a clearer segregation of business responsibilities and operations for PCB’s existing automated solution business, thereby enabling the respective management teams to focus on opportunities specific to each of the automated solution business; (iii) The Proposed Listing is expected to unlock shareholders’ value in the automated solution business and provide a transparent valuation benchmark for the same in Hong Kong; and (iv) The Proposed Listing will provide the Company and its automated solution business with a diverse fund raising platform in the future i.e. Hong Kong equity capital markets, which in turn will increase its financing flexibility to fund its future growth.

3. ADVISERS AND OTHER REGULATORY REQUIREMENTS The Board has appointed Altus Capital Limited, a corporation licensed by the Securities and Futures Commission of Hong Kong to carry out Type 4 (advising on securities), Type 6 (advising on corporate finance) and Type 9 (asset management) regulated activities under the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong), as the sponsor for the Proposed Listing in Hong Kong (“HK Sponsor”). The Company has also appointed other professional advisers for the purpose of advising on the Proposed Listing.

The Board wishes to highlight to the shareholders of the Company (“Shareholders”) that the Proposed Listing is at a preliminary stage and fairly extensive preparatory work is required and that such preparatory work may involve an uncertain time frame.

The Proposed Listing is also subject to, among others, satisfactory due diligence and assessment of suitability for listing by the HK Sponsor and other professional advisers, approvals being obtained from the relevant authorities in Hong Kong and Malaysia (where required), as well as the Shareholders at an extraordinary general meeting to be convened. In addition, the Proposed Listing is subject to assessment of other factors such as general economic and capital market conditions. There is no assurance that such approvals would be granted or that the Proposed Listing may occur. Therefore, Shareholders should note that the Proposed Listing may or may not materialise.

The Company will make further announcements in relation to the Proposed Listing, as and when appropriate, under the Main Market Listing Requirements of Bursa Malaysia Securities Berhad.

This announcement is dated 13 June 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 19-6-2017 06:33 AM

|

显示全部楼层

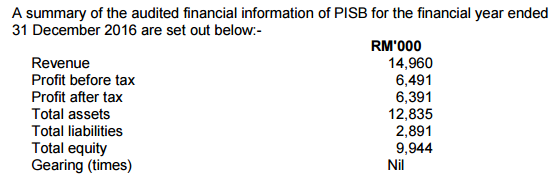

Type | Reply to Query | Reply to Bursa Malaysia's Query Letter - Reference ID | IQL-14062017-00002 | Subject | ACQUISITION OF REMAINING 40% SHAREHOLDING IN PENTAMASTER INSTRUMENT SDN BHD ("PISB") ("ACQUISITION") | Description | Acquisition of remaining 40% shareholding in Pentamaster Instrumentation Sdn. Bhd. | Query Letter Contents | We refer to your Company’s announcement dated 9 June 2017, in respect of the aforesaid matter. In this connection, kindly furnish Bursa Securities with the following additional information for public release:- 1. The prospects of PISB. 2. The estimated time-frame to complete the Acquisition. 3. The Company's cost of investment in the 60% equity interest in PISB that it currently holds, and the date(s) of investment. 4. To state whether PISB is a major subsidiary. 5. Whether any comparison and valuation has been taken into consideration in arriving at the purchase consideration for the Acquisition. If yes, the details thereof. | Unless stated otherwise, definitions used in this announcement shall carry the same meaning as defined in the announcement dated 9 June 2017 in relation to the Acquisition.

With reference to Bursa Malaysia Berhad’s query letter dated 14 June 2017 (Reference Number: IQL-14062017-00002), the Board of Directors of PMCB wishes to inform/clarify the following:- 1. The prospects of PISB. The Company anticipates the demand for PISB’s Test and Tune Solution Equipment to grow in the remaining quarters of year 2017 and contribute positively to PMCB Group.

2. The estimated time-frame to complete the Acquisition. The documents for the transfer of the Shares have been executed and the consideration for the Shares have been satisfied on 9 June 2017. Accordingly the Acquisition was deemed completed as of 9 June 2017.

3. The Company’s cost of investment in the 60% equity interest in PISB that it currently holds and the date(s) of investment. The Company’s 60% equity interest in PISB, represented by 180,000 ordinary shares, were allotted to PMCB on 19 July 2004 at a cost of RM180,000.

4. To state whether PISB is a major subsidiary. PISB is not a major susidiary of PMCB.

5. Whether any comparison and valuation has been taken into consideration in arriving at the purchase consideration for the Acquisition. If yes, the details thereof. Other than the shares allotted to PMCB in 2004 as stated above, the Company has not acquired or disposed of any share in PISB. The Company was therefore not able to make any meaningful comparison of price for the Shares. In arriving at the purchase consideration for the Acquisition, the Company did not undertake an independent valuation of the Shares. However, being the majority shareholder of PISB with access to its financial statements, the Company carried out an internal valuation to gauge the current net asset value of the Shares as the main basis for negotiating and arriving at the purchase consideration taking into consideration the current NAV of PISB and its earning contributions going forward.

This announcement is dated 15 June 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-6-2017 12:18 AM

|

显示全部楼层

Type | Announcement | Subject | OTHERS | Description | PENTAMASTER CORPORATION BERHAD (PCB OR THE COMPANY)- INCORPORATION OF A WHOLLY-OWNED SUBSIDIARY COMPANY | Further to the Company’s announcement dated 13 June 2017, the Board of Directors of PCB wishes to announce that Pentamaster International Limited (“PIL”) was incorporated in the Cayman Islands on 12 June 2017 as a wholly-owned subsidiary of PCB. The Certificate of Incorporation was received by the Company on 19 June 2017.

PIL was incorporated under the Cayman Islands Companies Law (2016 Revision) as an exempted company with limited liability with an authorised share capital of HKD380,000 divided into 38,000,000 ordinary shares of HKD0.01 each (“PIL Shares”) and an issued and paid-up share capital of HKD0.01 divided into 1 PIL Share. The principal activity of PIL is investment holding.

This announcement is dated 19 June 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 18-7-2017 01:13 AM

|

显示全部楼层

本帖最后由 icy97 于 18-7-2017 03:38 AM 编辑

腾达科技内部重组

8677万转让3子公司

2017年7月18日

(吉隆坡17日讯)腾达科技(PENTA,7160,主板科技股)展开内部重组,以总值8677万6487令吉,把3家独资子公司股权,转给Pentamaster国际有限公司(PIL)。

腾达科技今日向交易所报备,从事自动化解决方案业务的3家子公司分别是Pentamaster科技(马)私人有限公司(PT)、Pentamaster Equipment 制造私人有限公司(PQ)及Pentamaster Instrumentation私人有限公司(PU)。

注入Pentamaster国际香港上市

完成后,Pentamaster国际将直接持有3家子公司所有股权,并将在香港上市。

此外,腾达科技将以2550万令吉,把PIL的7.4%股权,脱售给GEMS Opportunities Limited Partnership。

GEMS Opportunities Limited Partnership是一家私募基金,主要投资在计划,在亚洲上市的公司。

如无意外,预计上述活动将会在今年第三季完成。

上个月,腾达科技指出,正考虑将分拆旗下自动化解决方案业务,到香港交易所主板上市。

当时,腾达科技也说,会把涉及自动化解决方案业务的子公司进行重组。【e南洋】

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

NON RELATED PARTY TRANSACTIONS | Description | Pentamaster Corporation Berhad ("PCB" or the "Company")Proposed Listing of the Company's Automated Solution Business on the Main Board of the Stock Exchange of Hong Kong Limited ("HKEX") ("Proposed Listing") | We refer to the Company’s announcements dated 13 June 2017 and 19 June 2017. Pursuant to the Proposed Listing, the Board of Directors of PCB (“Board”) wishes to announce that the Company had on 17 July 2017 entered into the following sale and purchase agreements to:

(i) undertake an internal reorganisation exercise within the Company and its subsidiaries (“PCB Group”) via the transfer of its entire equity interest in three (3) wholly-owned subsidiaries of the Company under the Automated Solution Business (as defined below) to Pentamaster International Limited ("PIL"), a wholly-owned subsidiary of PCB (“SPA I”) (“Internal Reorganisation”); and

(ii) dispose 74 ordinary shares of HKD0.01 each in PIL (“PIL Share(s)”), representing 7.40% of equity interest in PIL, after the Internal Reorganisation, to GEMS Opportunities Limited Partnership (“GEMS”), for a total cash consideration of RM25,500,000 (“Disposal Consideration”) (“SPA II”) (“Proposed Disposal”); (collectively referred to as “Proposals”).

Details of the Proposals are set out in the attached file. |

http://www.bursamalaysia.com/market/listed-companies/company-announcements/5488277

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-7-2017 01:08 AM

|

显示全部楼层

Type | Announcement | Subject | TRANSACTIONS (CHAPTER 10 OF LISTING REQUIREMENTS)

NON RELATED PARTY TRANSACTIONS | Description | PENTAMASTER CORPORATION BERHAD ("PCB" OR THE "COMPANY")PROPOSED LISTING OF THE COMPANY'S AUTOMATED SOLUTION BUSINESS ON THE MAIN BOARD OF THE STOCK EXCHANGE OF HONG KONG LIMITED ("HKEX") ("PROPOSED LISTING") | (Unless otherwise defined in this announcement, all terms used herein shall have the same meaning as those defined in the announcement dated 17 July 2017.)

Further to the announcement on 17 July 2017, the Board wishes to announce that the Internal Reorganisation has been completed on 21 July 2017.

This announcement is dated 21 July 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-7-2017 01:09 AM

|

显示全部楼层

Type | Reply to Query | Reply to Bursa Malaysia's Query Letter - Reference ID | IQL-20072017-00001 | Subject | PROPOSED LISTING OF THE COMPANYS AUTOMATED SOLUTION BUSINESS ON THE MAIN BOARD OF THE STOCK EXCHANGE OF HONG KONG LIMITED (HKEX) (PROPOSED LISTING) | Description | PENTAMASTER CORPORATION BERHAD (PCB OR THE COMPANY)PROPOSED LISTING OF THE COMPANYS AUTOMATED SOLUTION BUSINESS ON THE MAIN BOARD OF THE STOCK EXCHANGE OF HONG KONG LIMITED (HKEX) (PROPOSED LISTING) | Query Letter Contents | We refer to your Company’s announcement dated 17 July 2017, in respect of the aforesaid matter. In this connection, kindly furnish Bursa Securities with the following additional information for public release:- 1. The breakdown of proceeds for staff and other general administrative and operating related expenses and the details of the general administrative and operating related expenses. 2. The details of the proceeds in relation to the sales and marketing expenses. 3. The proposed utilisation by Pentamaster Corporation Berhad ("PCB") of the RM15 million upon reimbursement by Pentamaster International Limited. 4. The quantification of the total bank borrowings of PCB Group as at latest practicable date. 5. The date and cost of investment in the 7.4% of Pentamaster Technology (M) Sdn Bhd, Pentamaster Equipment Manufacturing Sdn Bhd and Pentamaster Instrumentation Sdn Bhd that is being disposed to GEMS Opportunities Limited Partnership ("GEMS"). 6. The corporate structure of the PCB Group after the completion of the Internal Reorganisation and Proposed Listing. | With reference to Bursa Securities's query letter dated 20 July 2017, kindly refer to the attached file for the Company's reply. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-7-2017 02:00 PM

|

显示全部楼层

本帖最后由 icy97 于 27-7-2017 08:24 PM 编辑

PENTA(7160)腾达科技 - 百忍成金,PENTA继续涨涨涨~~

27 Jul 2017

http://wesharenwetrade.blogspot.my/2017/07/penta7160-penta.html

百忍成金是一句成语,释义是形容忍耐的可贵。另一个套用在股市的说法是,你买了一只好股票后忍耐不卖坚守上百天后,股票会变成宝贵的黄金了。(开玩笑的,笔者疯言疯语。)

不过其实也是有一点小道理啦,你买房产愿意等好几年让它建好或市值上涨,在股市中难道你不能付出一些些忍耐守住你的好股吗?

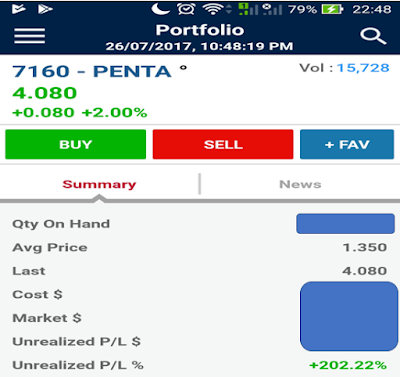

今天要与大家分享的喜悦是笔者持有PENTA纸上盈利达200%以上啦!!!

PENTA的旅程

去年11月18日以RM1.35买入。

3月31日,收市RM2.78 (第一番,历时133天)

7月26日,收市RM4.08 (第二番,历时117天)

这一路走来并不容易,因为:

一:PENTA目前没有派股息的习惯,所以心态上要说服自己不急于套利。

二:PENTA属于股价波动蛮大的一只上升股。股价上升快速,下降速度也相当快,少一点定力就会受股价波动影响而想卖出套利了。

开了二番代表笔者心态很好吗?其实还好,坚持守住是因为笔者研究其基本面相当看好其前景。可是问题是,笔者如此看好,却没有加码!!笔者知道自己的心理素质还不够强大,加码会大幅度提高自己的平均价成本,在心态上会更难不受股价波动影响。

喜悦分享完毕,相信大家也对PENTA的近况有所兴趣吧,因为近期PENTA内部动作频密,大家都想知道这对投资者是利好还是利空呢?

PENTA的近况

6月15日:以RM6million增持40%股份于PU子公司,使其成为100%股份的独资子公司。

7月份:设立新的子公司-PIL,并把三个100%股份的独资子公司(分别为PT,PQ, PU,这三家子公司基本上就是完全贡献PENTA的净利)入注于PIL,以让PIL可以在香港上市。另外,出售PIL 7.4%的股份给一个投资机构。

因为之前已经写过PENTA收购子公司的看法了,而PIL要在香港上市的详情还没出炉,这里只简短的说明我的看法:

1. PENTA增持40%股份于PU子公司,价格是便宜到不行,而且可让净利增加,因此是利好消息。

2. PENTA入注3家子公司于PIL。因为股份不会再是100%了。假设PIL上市后,PENTA只持有PIL 60%股份,这些子公司40%的净利就不在归属于PENTA的账目了。这是对净利短期的影响。PIL在香港上市,就是IPO,会获得一笔资金,PENTA在IPO会获得多少资金,IPO的价格是多少,PENTA如何运用这笔资金等这些关键的细节暂时还不详,因此笔者先归类于中和消息。

3. 出售PIL 7.4%的价格给一个投资机构,价格是以P/E 10.4倍为估算。虽然PENTA从中可获利RM20million左右,可是看看PENTA目前的P/E,是19倍,所以这宗交易是卖得相当便宜的。不过该机构是作为strategic investors的作用,卖得便宜是无可厚非,而且出售7.4%的股份不是说太多啦,而且PENTA需要利用这笔资金大部分用作香港上市费用。

总结:敬请留意接下来PENTA对PIL在香港上市的细节公布,笔者是相当期待PENTA会如何利用这笔IPO获得的资金来扩充这个目前火热的自动化行业呢?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 27-7-2017 03:02 PM

|

显示全部楼层

本帖最后由 icy97 于 27-7-2017 08:25 PM 编辑

福布斯亚洲“营收10亿美元以下200强”

MyEG蝉联 5马企入榜

2017年7月27日

http://www.enanyang.my/news/20170727/福布斯亚洲营收10亿美元以下200强-myeg蝉联-5马企入/

(新加坡27日讯)福布斯亚洲今日公布2017年“营业额10亿美元以下200强企业”(Best Under A Billion)名单,大马共有5家企业上榜。

这包括艾尔软体(ELSOFT,0090,主板科技股)、Kerjaya(KERJAYA,7161,主板建筑股)、MyEG(MYEG,0138,主板贸服股)、腾达科技(PENTA,7160,主板科技股),以及伟特机构(VITROX,0097,主板科技股)。

福布斯亚洲在亚洲1万8000家公司,依据过去12个月和3年的营业额和盈利增长,以及5年投资回酬率,遴选出200家年度营业额介于500万至10亿美元(约2026万至令吉至40.51亿令吉)、有净利,且至少上市1年的企业。

2016年,我国同样有5家公司入榜。

今年入榜的大马企业中,MyEG已是连续第二年入榜。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 19-8-2017 12:22 AM

|

显示全部楼层

本帖最后由 icy97 于 21-8-2017 06:34 PM 编辑

Pentrox = Penta + Vitrox 的前身今世

August 17, 2017

Morgan Lim 反思者

读者们大家好, 笔者隔了好久没有题材可写,现在终于可以继续和大家分享分享。

不知道大家过得好吗?

笔者很幸运的,今年最大的持股Vitrox,第二大的是Kerjaya和第三大的Penta都有不错的回报。

笔者这个文章的目的就是为了和大家分享笔者最近从一个前辈身上学到的知识。那就是关于马来西亚Vision Inspection Automation Sector 这个行业的历史。

让我们从头开始,应该在十年前吧,这个行业一开始是由KeysightCorporation负责最赚钱的Software和 algorithm部分,由Vitrox负责Software 的 maintenance,而Penta负责的则是整个Hardware的部分。当时,Vitrox和Penta都只是很小的企业,都只是Keysight的subcontractor,也就是说Keysight只做最赚钱的部分,把不太赚钱的都给别人做。也就这样,Vitrox慢慢的从maintainance中学会了那些software的来龙去脉。

这一切维持到2009年的5月1号,Keysight确定退出这个Vision Inspection Automation Sector,把整个software的部分都卖给了Vitrox。所以现在呢,Vitrox可是整个Vision Inspection Automation的龙头,而Penta也还是一样负责Hardware的部分,负责制造整个机器出来。从前辈那边知道说,其实制造那个机器出来只需要买齐全部材料来组装,不会很复杂,最难的是software的部分,如何用高科技来帮助电板生产商(PCB manufacturer)省钱,省时及高品质地test产生出来的电板。

看回几个月前的文章,当时期待要和公司以前成长到300 million的revenue,当时还大概做了一些算法 觉得股价去到rm6应该可以达到,哪知道,就以今天的股价,若还没有bonus issue的话,股价已经高达rm 9.60,也大大出乎了我的预测。

Penta呢则是笔者前两个月这样才刚买的,虽然已经这个股票已经在今年起了大概150%,笔者在深入研究后,发现公司还有很大的成长空间。公司的director在今年中说了今年会有double digit growth。笔者也深信penta还有很大的成长空间因为公司有三个主要的部门,而有一个部门在那边拖后腿,不止没赚钱,还亏钱啊!但深加研究看,这个部门可是smart home segment,试想想,多几年smart home一定是每个新家都必须拥有的科技,所以公司还是可以继续成长下去的。

接下来让我们看看最值得大家注意,让大家振奋的!

若大家去比较Vitrox 2016和2015年的annual report,你们会发现多了一个35%的holding bhd,当时我还以为vitrox有acquisition开心极了,哪知,深加研究后,才看见这个消息。虽然知道得慢,但是这可让我对pentrox信心加倍呢。

Penang Automation Cluster

In line with the growth in these global markets, I am pleased that ViTrox Corporation Berhad, Pentamaster Technology (M) Sdn Bhd and Walta Engineering Sdn Bhd has formed Penang Automation Cluster Sdn Bhd (PAC), a joint venture partnership.

The cluster aims to create a first world-class SME precision metal fabrication cluster zone in Malaysia as a one-stop metal parts supply chain hub through collaborative efforts between local large companies (LLCs) and small medium enterprises (SMEs), which will attract attention of multinational corporations (MNCs) into this one-stop metal parts supply chain hub.

Expected Outcome

It is estimated that the cluster will achieve a total local large companies's revenue of RM980 million by 2021, and the spillover effect to the 18 SMEs under the cluster is estimated to be more than RM118 million. ------------------------------------------------------------------------------------------------------------ 简单来说呢就是,VITROX,PENTA和Walta 这三家公司将会在penang合作成立一个金属制造集群,在这个automation行业大展拳脚。和别的大小企业合作来成为一个全球高水准的金属零件供应商。而这个集群将又Vitrox的director带领。这个集群估计在2021年将可以达到高达980million的revenue,而有大约118million的revenue将会惠及这个集群的18间小型企业。 笔者也不了解这个集群实际会对pentrox有多少的利益,但从这边我们可以看得出,automation的龙头绝对就是pentrox了。接下来的人力费用肯定越来越高,automation也必定还有很长的路可以继续走下去。

额外的好消息也就是说,笔者持有的penta, kerjaya 和vitrox都被选进了FORBE’S 的asean选股。这也证实了这三家公司的潜力和品质。笔者还真是幸运,希望接下来的年里也可以选出和FORBE'S 一样的好股票。

笔者想和大家分享一个非常另类的想法,笔者在买入这三家股票时,当时这三家股票都在高点。笔者做完功课后和大家分享,大家都说股价已经起了那么多,不能买了,而笔者就自己买了。买了之后就持有至今,也都拥有了不错的回报。当然也有些股票买了后跌到止损点就卖出的,但我想提出的看法是这个。股价会起的大致上都是好公司,股价会跌的都是些不太好的公司。而我们人类都会有过度保护自己的意识,都买一些股价跌了的不好的公司,好的公司却不敢追了,不舍得付出更高的价钱来买高品质的公司。 (这边没有教大家追高而把自己曝露在高风险的情况,请不要误解和批评。只是笔者在反思这个问题,个人是觉得若做足了功课,所谓"水至清则无鱼,股至清则无疑",请大家设了止损点后,给自己一个机会拥有更好的公司,说不定会有不同的体会。)

每个企业家都必定经过不少的挫折和失败,也一定会在很多企业里失败。但他们的共同点就是他们在不断失败的企业累计经验和技术,直到最后拥有一个赚钱成功的企业,然后就紧紧守着这个企业,靠这个企业来成功。买股票又何尝不是这样,penta 和vitrox都是我向往的企业。我也深信这间公司将会为我带来可观的收获。

希望多年后,回首一看,看回这些文章,将会有更多的感触。感激现在的付出,感激现在孜孜不倦的学习,方可以在以后拥有向往的生活。

纯属分享,没任何买卖意见。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 21-8-2017 02:19 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 24-8-2017 06:27 PM

|

显示全部楼层

本帖最后由 icy97 于 24-8-2017 08:48 PM 编辑

SUMMARY OF KEY FINANCIAL INFORMATION

30 Jun 2017 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 30 Jun 2017 | 30 Jun 2016 | 30 Jun 2017 | 30 Jun 2016 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 54,811 | 38,848 | 102,383 | 67,447 | | 2 | Profit/(loss) before tax | 11,768 | 8,554 | 21,109 | 12,792 | | 3 | Profit/(loss) for the period | 10,316 | 7,245 | 18,811 | 10,647 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 10,274 | 6,664 | 17,812 | 9,833 | | 5 | Basic earnings/(loss) per share (Subunit) | 7.01 | 4.57 | 12.15 | 6.94 | | 6 | Proposed/Declared dividend per share (Subunit) | 0.00 | 0.00 | 0.00 | 0.00 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.8527 | 0.7382

|

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

3489

3489  112

112